HOW FAR CAN THE FED GO?

By Alexandre Hezez, Groupe Strategist

Editorial

There is no doubt about it, Jerome Powell would like to be remembered as a second Paul Volcker rather than a second Arthur Burns (Fed Chairman from 1970 to 1978), now admitting that his fight against inflation could trigger a recession. The Fed chairman pledged to ‘keep at it until the job is done’, referring to Volcker’s book, ‘Keeping at it’.

As a result, the door is open to all assumptions regarding future rate hikes and the market fears the worst. When Carter appointed Volcker to the Fed’s management (July 1979), the Fed decided to reverse US monetary policy. Volcker policy’s resulted in interest rate hikes and, consequently, that of the dollar exchange rate: the nominal short-term interest rate rose from 7.4% in 1978 to 14% in 1981, the long-term rate from 7.9% to 12.9%. So the question is whether Jerome Powell’s normalisation has unlimited capacity. The US experienced a period of very high inflation in the 1970s, which lasted until the early 1980s. Price increases were close to 15% year-on-year. Jerome Powell evoked ‘what Paul Volcker and the Fed did to finally control inflation after several unsuccessful attempts’, stressing that ‘the public had come to consider inflation higher as the norm and expect it to continue’.

Firstly, what are the US Federal Reserve’s goals?

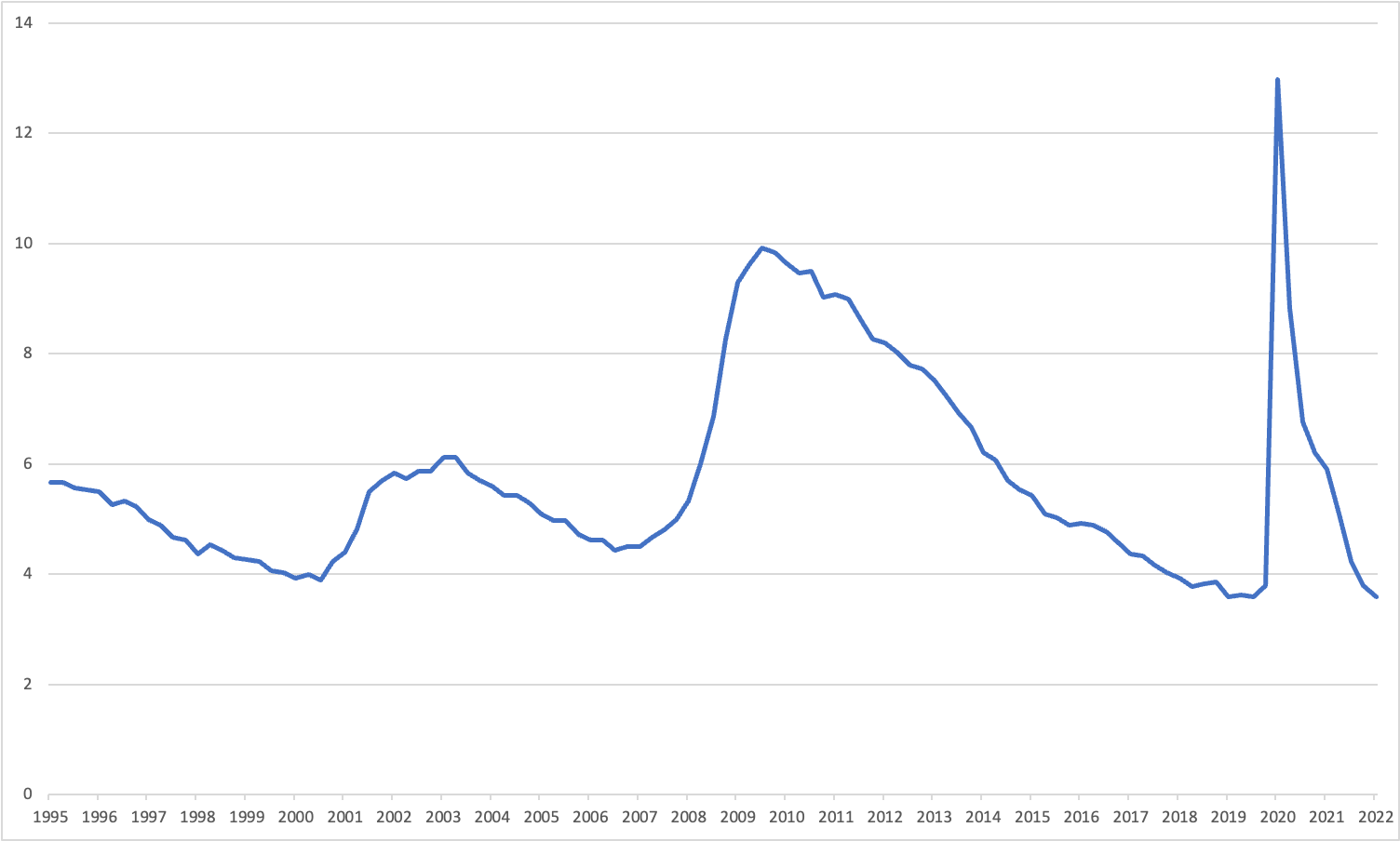

The longer inflation remains high over time, the greater the risk of it becoming entrenched. In response, the Fed will have to be even more hawkish to return it to a more reasonable level. Consumption is holding up for the time being. It is even putting up too much resistance for the Federal Reserve, which wants to slow inflationary catalysts in all their forms despite the ‘pain’ they could cause. Households strengthened their financial situation during the pandemic through public transfers, forced savings, and a robust labour market.

US unemployment rate

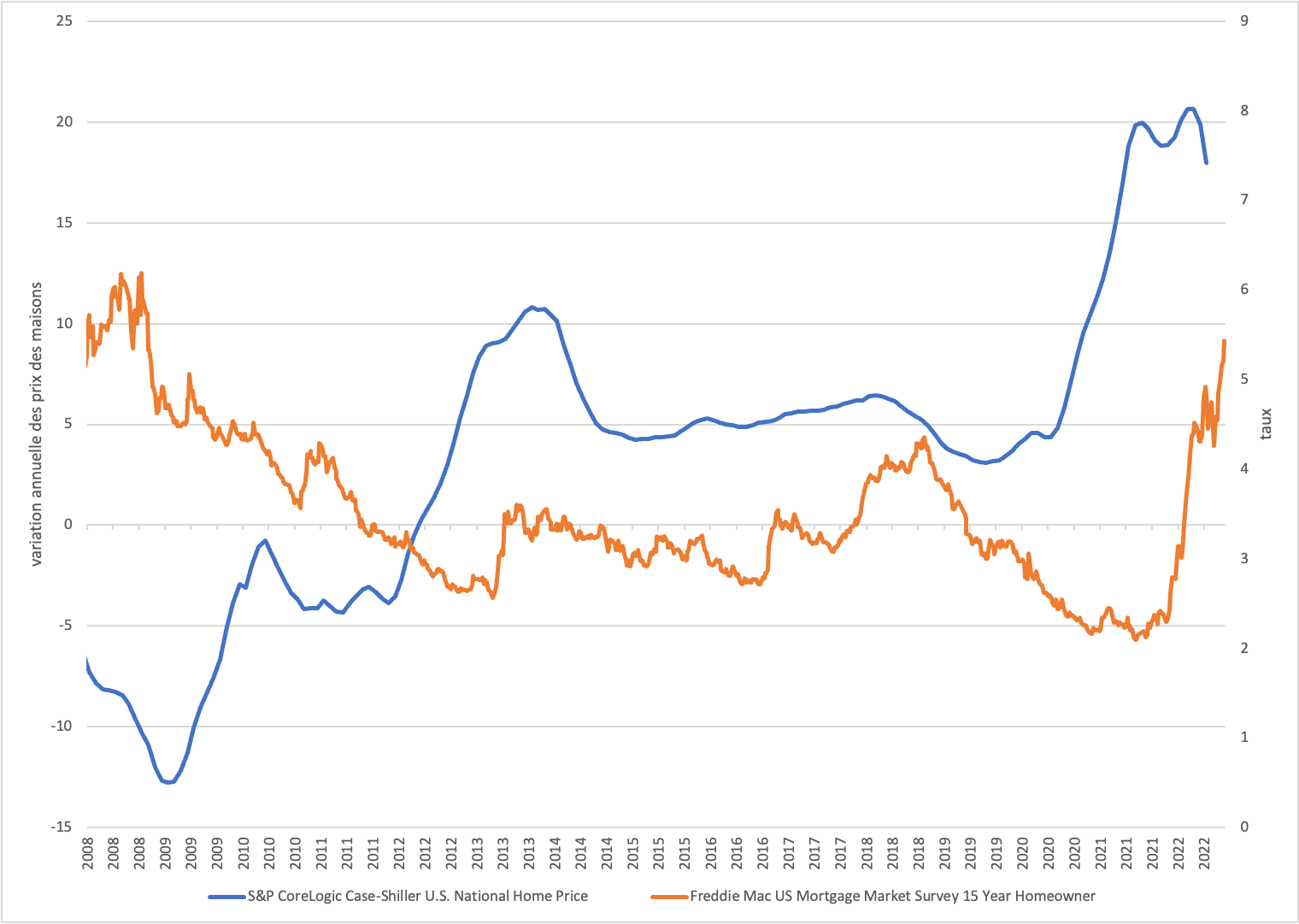

The real estate market has benefited from abundant liquidity since 2020. The S&P Case-Shiller US National Home Price Index, which tracks the nominal value of the residential real estate market in twenty US cities, has risen 44% since March 2020. Although this annualised hike of 17% amplifies the wealth effect, it is not without negative consequences. Rents and sales prices have risen on the back of the Fed’s historic liquidity facilities over the past two years. Indeed, the real estate-related component still contributes very positively to inflation due to a significant latency between the drop in activity (which started several months ago) and its effect on prices. The non-energy housing component (mainly rents) was 0.72% in monthly variation in August, which has been unheard of for 22 years! Real estate accounts for 32% of underlying inflation figures. This figure is significant and worrying because it shows that the ‘housing’ component can increase in proportions that have not been observed before.

Change in US house prices versus real estate rates

Stabilising or lowering real estate prices is difficult and obviously carries a substantial risk to growth and the financial system. The increase in mortgage rates was strong and rapid and should have significant effects in the coming months. The risk of a real estate crisis is possible, but we believe that we are in a completely different configuration than in 2006-2007. Mortgage debt remains under control and does not present a systemic risk for the banking system but an effect on consumption.

While there is a growing risk that stronger evidence of demand destruction will be needed to calm rate hike expectations, unemployment is likely to level off in the coming months. The labour market is expected to deteriorate in many sectors, including real estate, easing wage pressure.

The publication of Q2 results demonstrates a resilience of businesses in maintaining their margin. Q3 shows more heterogeneous situations, with more profit warnings in the sectors directly affected by macroeconomic weakness in Europe and Asia. Special attention should be paid to difficulties in passing on the price of inputs (commodities, wages) to turnover. The longer the inflationary situation continues, the more the consumer dam could give way, given the impact on their purchasing power and confidence.

Stagnating money supply and rate hikes should start to have an impact on the real estate sector and rebalance employment as a knock-on effect.

'We need to act forcefully as we have done, and we need to keep at it until the job is done

Jerome Powel - 8 september

Money supply variation over six months

Other deflationary catalysts are in motion

The unblocking of supply chains, coupled with the drop in the price of recent commodities and the Fed’s determination should still lead to macroeconomic conditions in the US that are less negative than expected if the reversal in inflationary pressures is confirmed. Financial conditions will continue to tighten. We expect unemployment to rise in the coming months. Global economic growth is deteriorating and commodities are on a downward cycle. Paradoxically, bad employment news should be a relief for markets that would like to see wage growth contained.

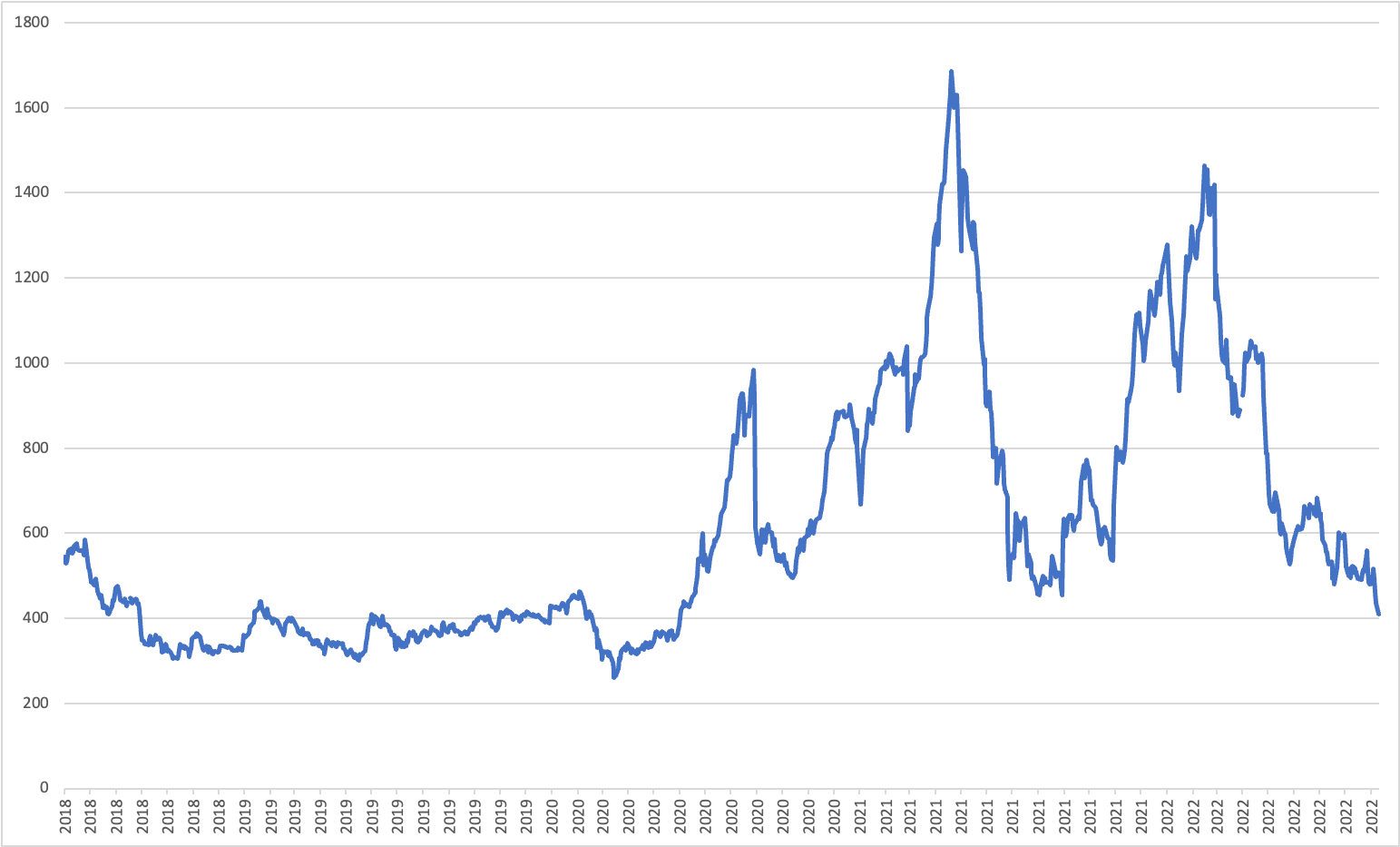

Price of a bushel of wood

Is the Fed going overboard?

Jerome Powell clearly wants to hurt businesses and households to bring inflation down. And the Fed has no choice because it is concerned about preserving its inflation credibility, as it did not foresee a rise in prices in 2021-2022. The most important thing is to keep inflation expectations reasonable (best indicator for its credibility) to avoid, as in the 70s, an extremely high period of unemployment in order to control it.

It should also be noted that debt levels are much higher than in the 70s. US government debt stood at 35% of GDP compared to 126% of GDP (Gross Federal Debt).

US federal debt and 10-year rate

The effects of rate hikes are multiplied, and Jerome Powell will not need to bring in levels of the same kind.

The Fed is not going overboard, its credibility is key to the future of the US economy. Time is running out and history warns against premature easing of monetary policy.

Paul Krugman, in his latest editorial, is right to insist that the Fed is acting to preserve this asset by trying to lower current inflation early enough for the public to maintain its belief in low future inflation.

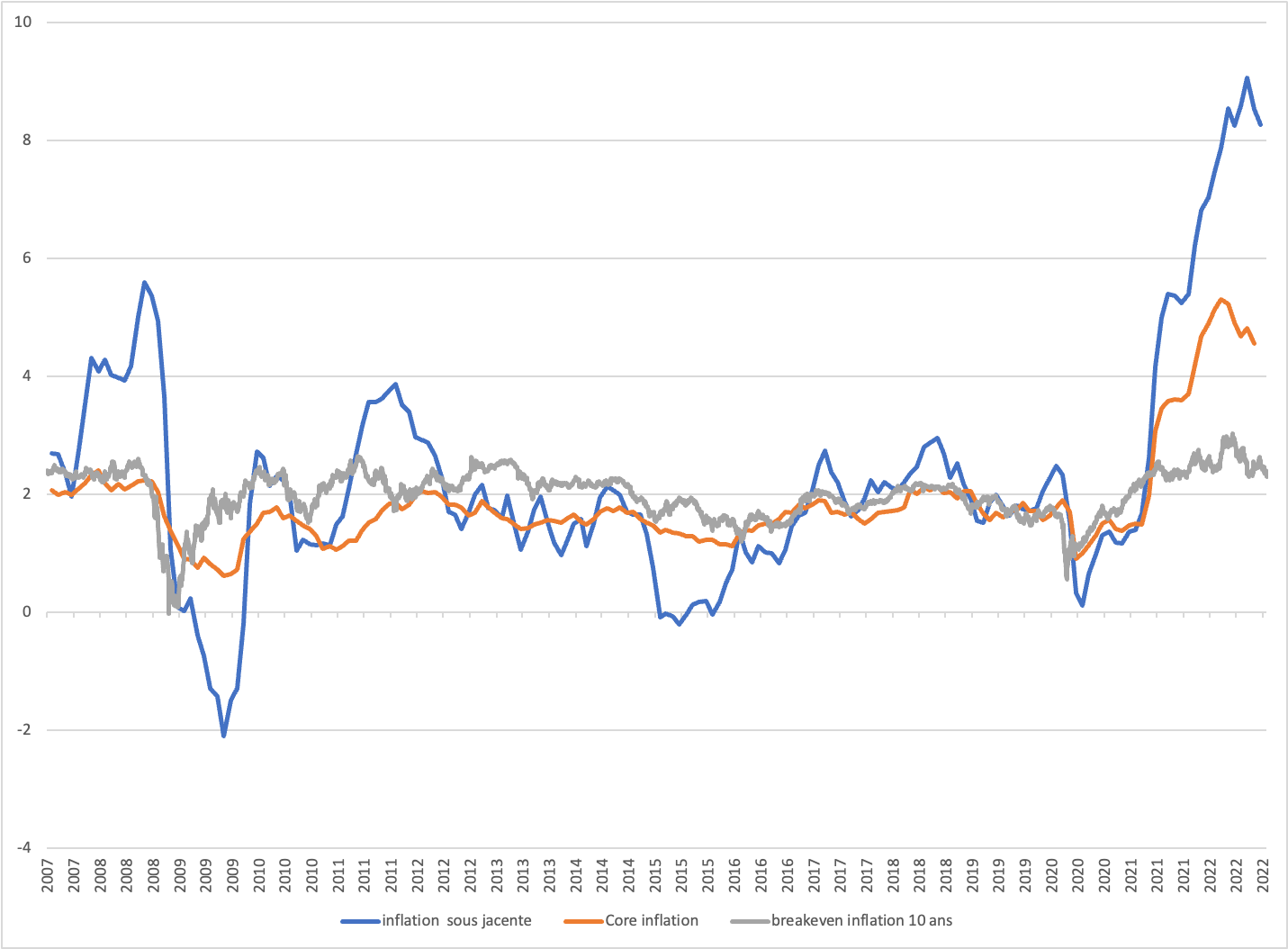

Headline inflation, non-energy inflation, 10-year inflation forecast

In the very short term, the risk would be to not do enough and be obliged to do even more in a few months time and anchor long-term expectations at a much higher level.

We now expect the Fed to stop at around 4.25%/4.5% as the balance sheet reduction also acts as a drag on financial conditions, equivalent to an additional 50 basis point rate hike over the year. Despite higher than expected figures in August, we continue to believe that clearer signs of disinflation will emerge in the US by the end of the year, particularly in the November report.

As soon as we have clear evidence that prices are falling, volatility will decrease in the US and the Fed will have been right. Otherwise, the Central Bank will have to go even further and the assets, as a whole, will adjust.

Convictions

A soft landing of the global economy looks increasingly unlikely given the acceleration of central bank rate hikes and the energy crisis. However, cases are well differentiated according to geographical area. Endogenous situations exist, such as in the USA with the overheating of the economy or in China with the real estate crisis. At the same time, there is an exogenous crisis, as in Europe, with gas and the situation in Ukraine.

In the USA, the consumer situation continues to demonstrate a form of resilience obliging the Fed to take stronger action. We believe that the Fed remains very credible in its action and does not want to produce a wealth effect that would prove to be inflationary. Everything will be put in place to avoid the summer’s scenario of a strong rally in the financial markets calling its action into question. Many asset bubbles have already been cleared (SPAC, zombie companies, crypto assets, high leverage companies, etc.). Monetary normalisation is already in place.

In Europe, the situation remains very problematic. Crisis factors are exogenous to the area, but the energy shock is spreading through the economy. The ECB is far behind on its normalisation and needs to speed up, no matter what. German inflation will reach 10% in December. This normalisation is taking place in a downturn, and we are anticipating a recession which, unlike in the USA, is unlikely to bring down inflation rates as quickly as hoped. The Eurozone economy outperformed in the first half of the year due to increased demand following the lifting of Covid restrictions, however, the latest figures are much less encouraging. In Europe, the proximity of the conflict in Ukraine is still causing major uncertainties as winter arrives, due to energy supply. Sovereign spreads will remain under pressure. The political context is exacerbating threats. After Italy, numerous elections will test European solidarity (Latvia, Bulgaria, Lower Saxony, Slovenia, and Austria). At the end of the month, the EU summit will test EU unity, which is not infallible even in the face of the imminent danger of a war on its doorstep. Only a resolution of the conflict (unlikely at this stage) could be a catalyst for a reversal of sentiment.

Regarding shares, Q3 is at risk and suggests more heterogeneous situations, with more profit warnings in the sectors directly affected by macroeconomic weakness in Europe and Asia. Corporate margins will be challenged and stakeholders who have built their model on debt are in a situation that will worsen given the deteriorating financial conditions. Rising prices are weighing heavily on global demand, leading many businesses to cut or even stop production. The risk of recession is growing considerably as the situation for households and businesses continues to deteriorate For Europe, import price trends are up 30% year-on-year, while they are still under 10% for the USA. We continue to believe that US quality companies will benefit from their competitive situations. Major tech stocks are likely to come back in favour of investors given their balance sheets. Indebted businesses remain in an uncomfortable situation.

China is opening up again, but the outlook remains bleak. China is no longer a dream for investors. The drop in the epidemic curve has allowed the authorities to confirm the reopening of Chengdu, reinforcing China’s strategy to act earlier than in the past in order to avoid situations that are difficult and time-consuming to restore, such as Shanghai in the spring. Real estate sector difficulties are still prevalent and the authorities only provide calibrated support. However, consumer-focused schemes and a counter-current PoBC should support markets. The congress, the most important date in China’s political agenda, will provide clues as what direction the country will take in the coming years.

The Bank of Japan still has not adjusted its monetary tools to maintain pressure on interest rates and the currency, which should be favourable to shares in other areas.

It should be noted that hedging positions and index volatility remain very significant and the slightest piece of good news could lead to sharp reversals. We are maintaining our neutral stance on shares.

In terms of currencies, we remain negative on the GBP: the equation looks more unfavourable given the risk of a sharp increase in the UK’s double deficit over the coming quarters. Japanese Treasury intervention should contribute to a certain stability of the yen.

Regarding the dollar, we believed parity was adequate. At the end of the month, the dollar, led by the Fed, accelerated its rise. A more marked drop in US inflation should allow stabilisation. However, we believe that the USD remains the only safe haven against accelerating inflation or a globalisation of the Russia-Ukraine conflict. It is clear that the dollar’s bullish trend is negative on risky assets.

Regarding interest rates, profitability levels are becoming attractive again. In Europe, tensions are still to come, both in terms of spreads and sovereign spreads. Instead, we favour US assets for the coming months. Investment terms will be generally short. For the time being, we still recommend keeping a liquidity pocket.

The factors that would lead us to position ourselves more strongly on the market are a drop in employment and real estate figures in the US and, of course, a change in the Fed’s rhetoric. The monetary tightening cycle must finally be sufficient to bring inflation back in line with the central banks. The current situation must experience several developments more or less simultaneously in order for us to adopt a more positive view on risky assets.

In our central scenario, US disinflation should start, although a return to the pre-pandemic environment of very low and stable inflation is unlikely. Beyond geopolitical aspects and the specific European situation, US inflation will mark the future trend of the market as a whole.

Macroeconomic review

An air of Jean-Claude Trichet

The Jackson Hole Symposium highlighted the change in rhetoric and attitude of ECB members. Isabelle Schnabel held a tough line against inflation, championing ‘determination’ and ‘reacting more strongly to the current surge in inflation, even at the risk of lower growth and higher unemployment’. François Villeroy de Galhau confirmed the willingness and capacity to fulfil the ECB’s mandate by raising key rates beyond normalisation, if necessary. Forward guidance, progressiveness, and management of expectations relating to interest rates have thus been put on the back burner to return to pre-Draghi methods. To some extent, he updated Jean-Claude Trichet’s famous phrase, ‘We never pre-commit’. The ECB wants to regain its independence and credibility, regardless of the state of the economies or the needs of member countries. Like the Fed, the ECB will now act quickly and vigorously to reach a target rate with a second hike of 75 bp at the end of the month. The risk of recession should increase and materialise at the end of the year. However, this does not matter, indicators show that inflation is spreading in many areas and this spiral needs to be ‘broken’ or at least acted on, which is the ECB’s primary mission regardless of the political or economic situation. However, this situation is not without risk for the already fragile eurozone. The sovereign risk, which seemed to have ended in 2012, could reappear. Governments will therefore have to manage themselves this time, until they return to more suitable levels of inflation.

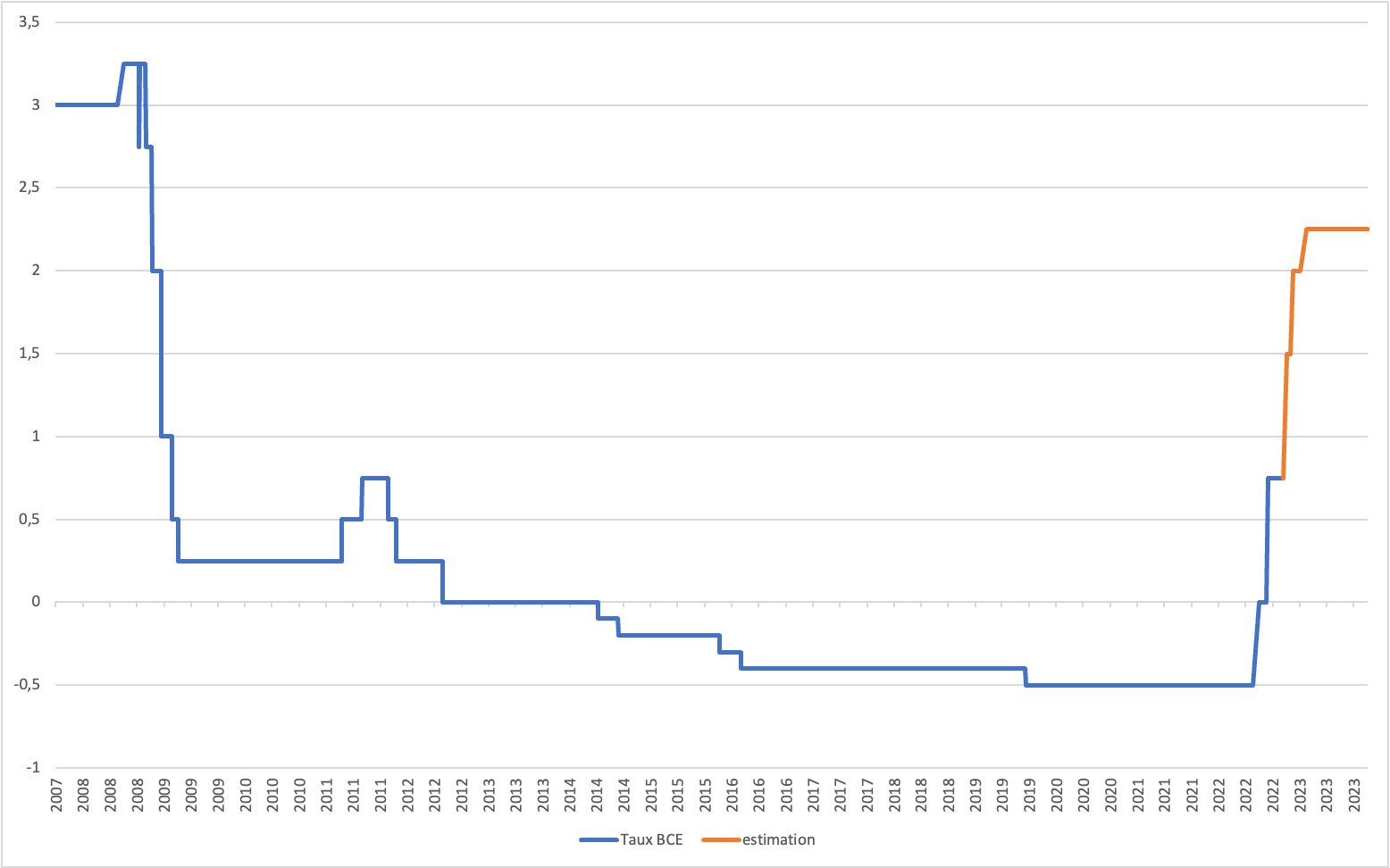

ECB rate

'Further decisive action is required to bring the inflation rate down to 2% in the medium term.

Joachim Nagel, President of the Bundesbank

The global economic slowdown is stronger than expected

Combined with the continuing effects of the COVID-19 pandemic, the war is slowing growth and adding to price tensions, especially for food and energy. Despite the catch-up effect following fewer COVID-19 infections worldwide, global growth should remain sluggish in the second half of 2022, before decelerating further in 2023 to an annual growth level of just 2.2%, according to the OECD. Global GDP is expected to be at least USD 2.8 trillion lower in 2023 than that forecast for December 2021 (before the war in Ukraine). The costs associated with the war in Ukraine are very diverse, but this amount gives an idea of its global price in terms of economic production. One of the main factors slowing global growth is the widespread tightening of monetary policies due to the greater than expected overshoot of inflation targets. China’s strict lockdowns accompanying the country’s zero COVID policy also had an impact on the Chinese and global economy. Business shutdowns and real estate market failures slowed China’s growth to just 3.2% in 2022. Significant uncertainty surrounds projections. More severe fuel shortages, especially gas, could reduce growth in Europe and thus global growth. Tax support is needed to help cushion the impact of high energy costs on households and businesses. However, short-term tax measures to reduce the cost of living should take into account the need to avoid a further persistent and therefore inflationary stimulus that would lead central banks to be even more restrictive. The tight labour market (with unemployment rates hitting or approaching 20-year lows) is boosting wages and helping to mitigate the loss of purchasing power and growth. That said, it is also contributing to widespread inflation. Wage growth has increased in many countries, particularly in the USA, Canada, and the UK, but not yet in the eurozone.

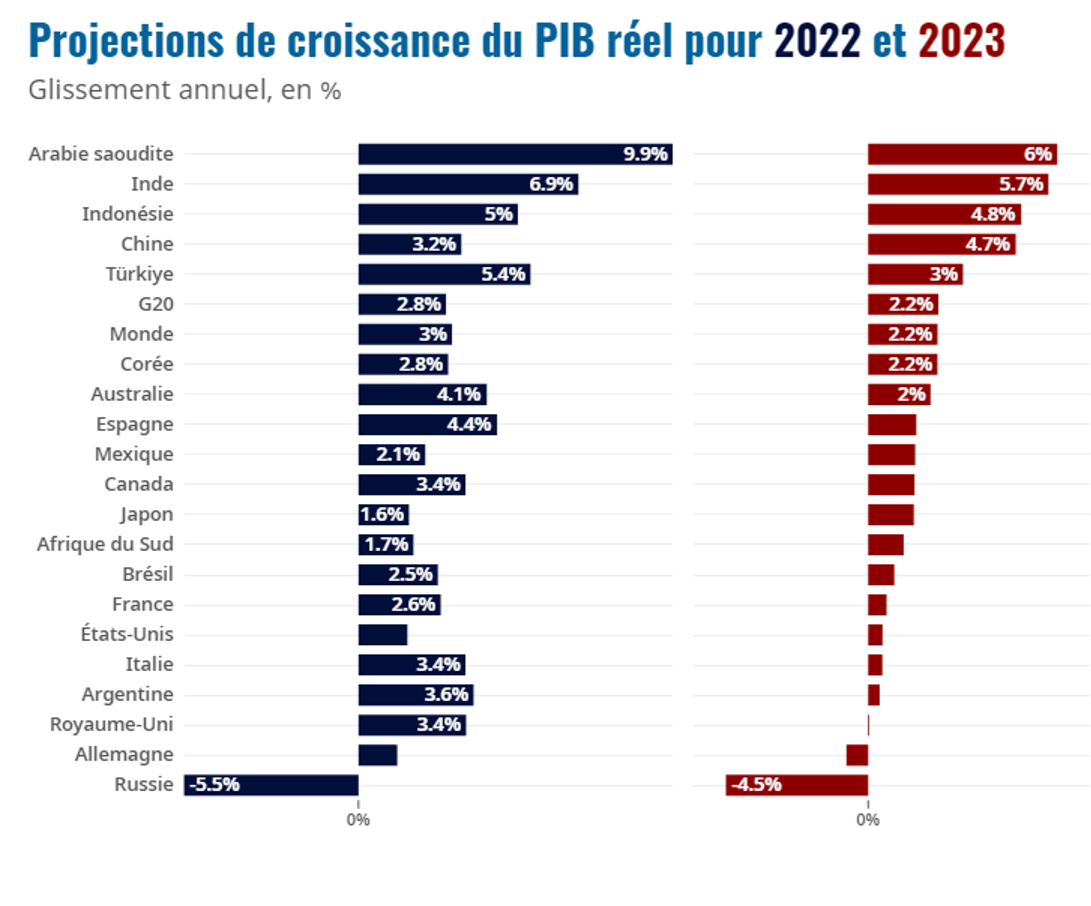

Real GDP growth projections for 2022 and 2023 (year-on-year; in %)

Market review

The European market, caught between the hammer of inflation and the anvil of recession

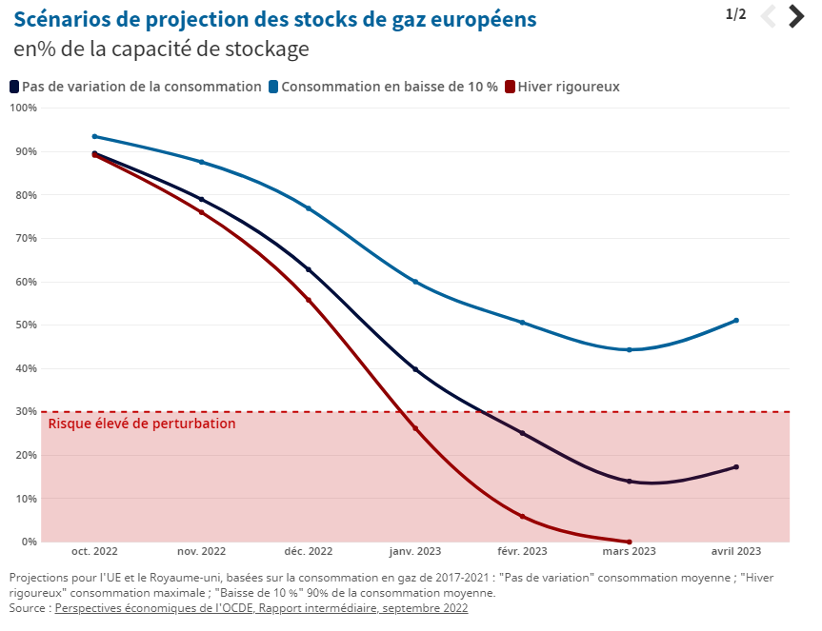

Overall, we remain cautious regarding Europe. Despite the accumulation of signs of a contraction in activity (PMI, IFO), messages from ECB members continue to be hawkish which should make it clear to businesses and workers that demand conditions will become less favourable. The eurozone is paying a heavy price for the war in Ukraine. Inflation data is more important than any other figure, and the ECB seems willing to accept weaker growth. The improvement in inflation will mainly come from stabilising energy prices and fewer bottlenecks as it is essentially an improvement on the supply side of the economy. We believe that rates have not reached a high point and that valuations remain fragile. The 2023 profit growth consensus for indices is not yet adjusted and deteriorations should amplify given the indicators put forward. The stronger dollar only provides a little support given supply difficulties. However, the biggest challenge is gas. Increasing shortages could dampen European growth by 1.25 points in 2023 and inflation in Europe could increase by 1.5 points. If the EU is unable to reduce consumption, stocks may prove insufficient to ensure that demand for a typical winter can be met without lowering them to critical levels.

Projection scenarios for European gas stocks (in % of storage capacity)

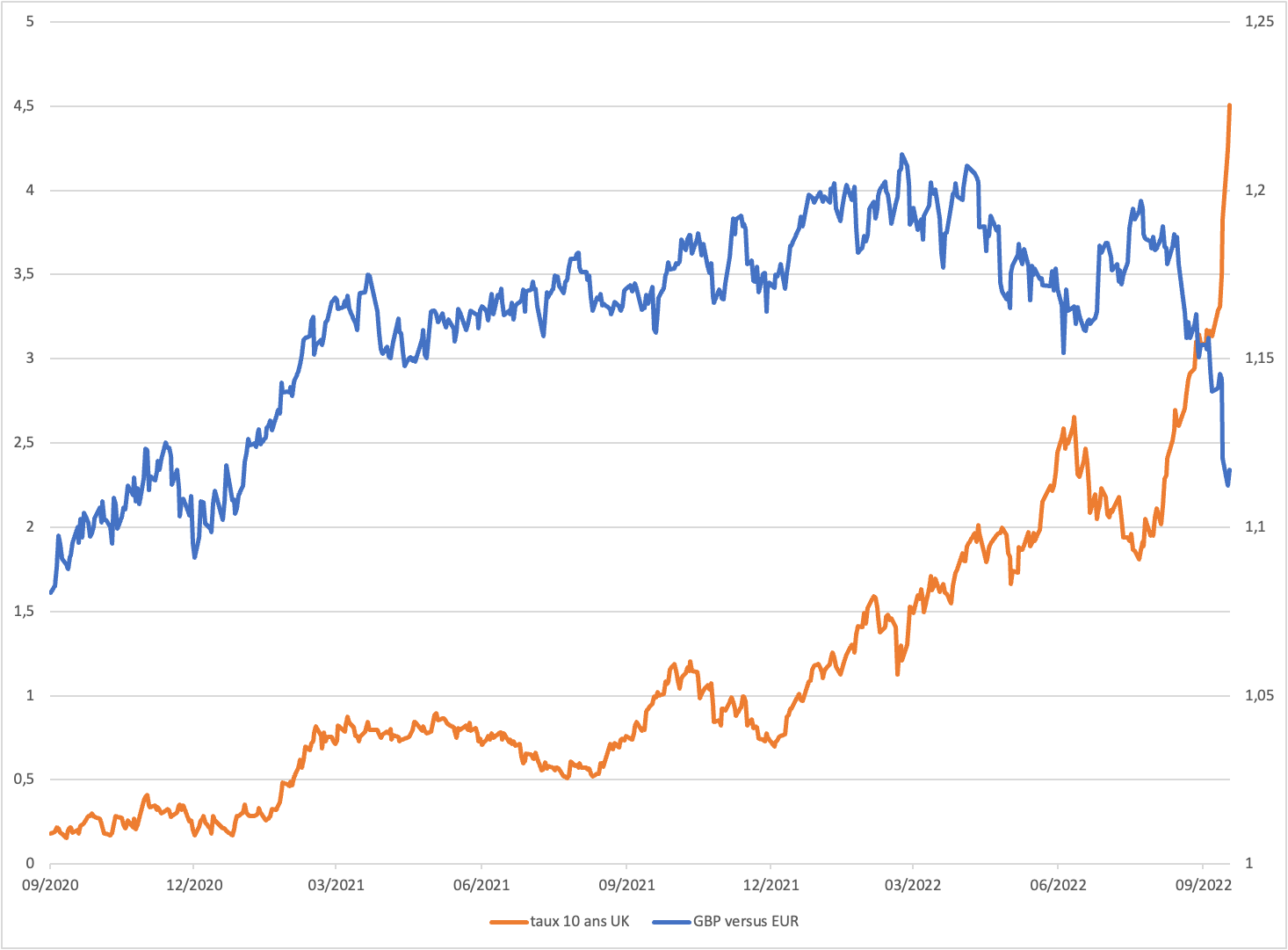

Pound sterling: the great dive

- A mechanism to freeze energy prices for households for two years and businesses for six months (cost estimated at 60 billion for six months);

- Tax cuts for the wealthiest households and businesses (45 billion by 2026);

- A reduction in purchase taxes to support the real estate sector.

The government’s goal is to support economic growth, which is showing signs of a slowdown, such as contracting PMIs, and to combat the strength of inflation linked to energy prices. However, such support under current inflationary circumstances is likely to continue to fuel price hikes and force the Bank of England to continue its monetary tightening. Against this backdrop, the risk of a widening double deficit (budget and external) resulted in downward pressure on the currency and upward pressure on interest rates.

Livre Sterling versus Euro - 10-year government rate

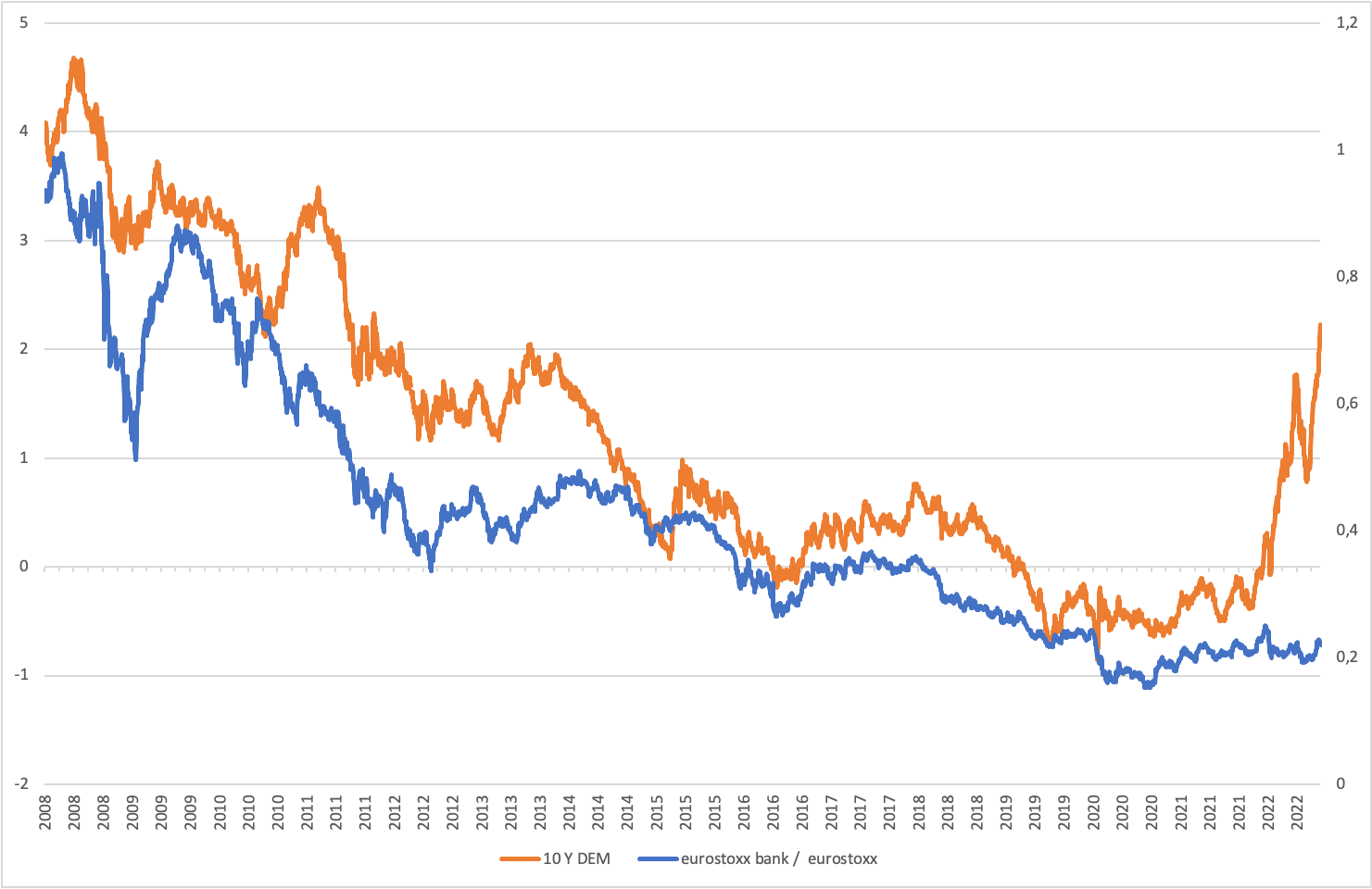

Banking & Insurance: welcome rate hikes

They remain fully aware that combined inflation/gas/interest rate shocks will have significant economic impacts. The banking sector remains one of the only sectors delivering rather optimistic messages. Banks are benefiting from the current rate hike environment (estimates are about 40 billion euros of additional income solely due to the rate effect). Provisions remain moderate, with banks lowering the risk of their balance sheets. All in all, this makes them much better equipped to cope with a recession. For the time being, risk management is under control and the efforts made over the years have strengthened their balance sheets and the operational side.

The insurance and reinsurance sector should also benefit from the environment. Between the increase in climate claims and the emergence of new risks, including the consequences of the war in Ukraine, the reinsurance sector is expected to experience a difficult 2022. However, reinsurers could raise premium rates within a ‘single digit’ percentage range during the key renewal season of1 January, given the pressures of inflation, the war in Ukraine, and the volatility of capital markets.

Eurotoxx bank/eurotoxx ratio versus German ten-year rate

Oil: less pressure, but for the wrong reason

The USA continues to draw on its strategic reserves in order to combat rising energy prices. However, despite geopolitical challenges regarding energy sources, the deterioration in the global economic outlook should affect oil prices. The combination of a stronger dollar and a lack of demand due to recession fears caused the price to fall. Furthermore, the OECD has revised its global growth forecast downwards for next year under the effect of consequences of the war in Ukraine that are more permanent than expected, particularly in the eurozone, and central bank interest rate hikes to contain inflation. China’s strict lockdowns accompanying the country’s zero COVID policy also had an impact on the Chinese and global economy. Business shutdowns and real estate market failures slowed China’s growth to just 3.2% in 2022. According to the IEA, China’s oil demand will drop 2.7% in 2022, the first drop since 1990. Additionally, Chinese refiners expect Beijing to release up to 15 million tonnes of oil export quotas for the remainder of the year to support exports, signalling a reversal in China’s oil export policy, increasing global supply, and lowering fuel prices. Global oil prices could remain below $100 USD/barrel for the remainder of the year as central bank rate hikes tightened credit and reduced investment in risk assets, such as commodities. US production should remain stable given the stabilisation in the number of rigs in operation. Demand for crude oil is expected to increase by 3.1 mbd in 2022 and 2.7 million bpd in 2023 to 100 and 102.70 mb respectively, according to Opep, which reviewed quotas to support prices.

Brent crude oil prices

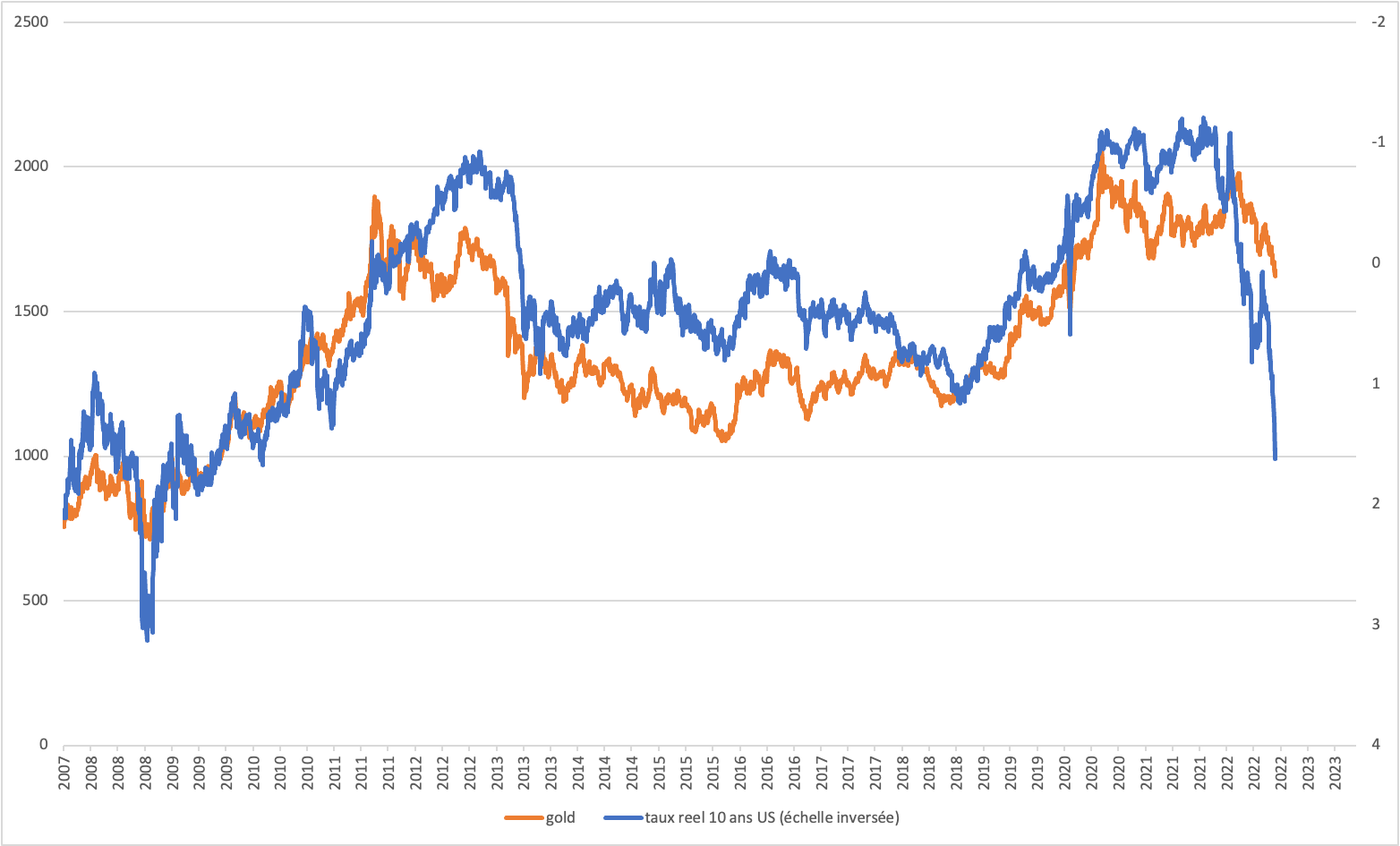

Gold: a safe haven, but not so safe this time around

In 2021, central banks continued to buy gold, with emerging countries becoming the main net buyers. Central banks around the world now hold over 35,000 tonnes of gold, representing about a fifth of all mined gold. Demand for gold from central banks reached record highs, pushing global gold reserves to their highest level in almost 30 years. However, while gold has traditionally been a safe haven, recent experience has shown that it has not benefited from geopolitical tensions.

The reason why we remain negative on gold is fundamental. Although we did not expect the US dollar to rise so sharply, it remains one of the factors explaining counter-performance. The main reason is still the Fed’s wish to slow the economy, which initially raised real rates to positive territory in March 2022. Gold prices stabilised at USD 1,750/1,800. The increase in real yields is penalising the lack of returns on gold in the eyes of investors outside of inflation considerations. Since then, as we expected, the rise in real rates has accelerated under the impetus of increasingly aggressive comments from FOMC members. The graph explicitly shows this empirical and academic relationship. When Janet Yellen, then FED chair, decided to raise real rates to slow real estate in 2013, gold experienced a period of dormancy until the end of 2018, when Jerome Powell decided to adopt a more accommodating monetary policy in the face of the recession risk linked to the customs conflict between the USA and China. Gold is clearly benefiting from the tensions which are preventing it from falling rapidly, but the rate now leads us to lower our target to USD 1,300. We do not expect a significant drop in real rates in the coming months. While gold is a long-term diversification option, the dollar remains a more appropriate safe haven.

Gold versus real rates (inverted scale)

Table of contents

Synthesis Strategy Richelieu Group - Author

Alexandre Hezez

Group Strategist

Disclaimer

This document was drafted by Richelieu Gestion, a subsidiary management company of Compagnie Financière Richelieu. In particular, this document may be based on public information. Although Richelieu Gestion makes every effort to use reliable and complete information, Richelieu Gestion does not guarantee that the information presented in this document is reliable and complete. The opinions and other information contained in this document are subject to change without notice.

The information, opinions, and estimates contained in this document are for information purposes only. No part may be considered as investment advice or a recommendation, canvassing, solicitation, invitation, or offer to sell or subscribe the securities or financial instruments mentioned. The information provided on the performance of a security or a financial instrument always refers to the past. The past performance of securities or financial instruments is not a reliable indicator of their future performance.

All potential investors must carry out their own analysis of the legal, tax, accounting, and regulatory aspects of each transaction, if necessary with the advice of their usual advisers, in order to determine the benefits and risks of the transaction as well as its suitability in view of its specific financial situation. The investor must not rely on Richelieu Gestion for this.

Finally, the content of the research or analysis documents or any excerpts appended or cited may have been altered, modified, or summarised. This document has not been drafted in accordance with the regulations intended to promote the independence of financial analyses. Richelieu Gestion is not subject to a prohibition on carrying out transactions in the securities or financial instruments mentioned in this document prior its publication.

Market data is from Bloomberg sources.

Pour aller plus loin

Monthly review – May 2024

Summary 1. Editorial: “The Fed’s Problem, Americans Are Too Rich!” 2. Macro-Economic Point 3. Asset Allocation: Prioritizing Flexibility in a Volatile Market 4. Asset Allocation

Monthly review – April 2024

Summary 1. Editorial: bubble or no bubble? that’s the question… 2. Macro: overly impressive figures? 3. Asset allocation: too early to worry? Editorial : Bubble

Monthly review – March 2024

China and the New World Disorder: Economic Stakes and Strategic Alliances Macro Point National People’s Congress 2024 Source : X In a world marked by