Summary

1. Editorial: “The Fed’s Problem, Americans Are Too Rich!”

3. Asset Allocation: Prioritizing Flexibility in a Volatile Market

The Fed’s Problem, Americans Are Too Rich!

Tweet about X on August 27, 2022

In August 2022, Jerome Powell made it clear: the fight against inflation would “cause pain for households and businesses” in the United States. Nearly two years after the historic interest rate hike, the sources of wealth for American households have never been more flourishing:

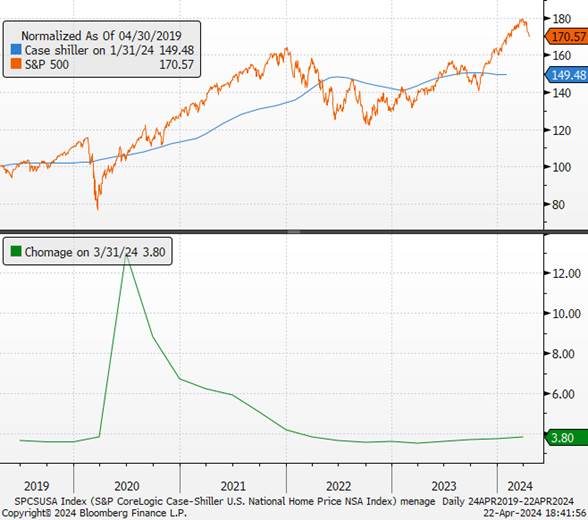

· Equities markets: they have reached historic highs,

· Housing prices: they are higher than ever,

· Unemployment rate: it remains extremely low.

Housing prices / S&P 500 / Unemployment rate

Sources : Bloomberg, Richelieu’s Group

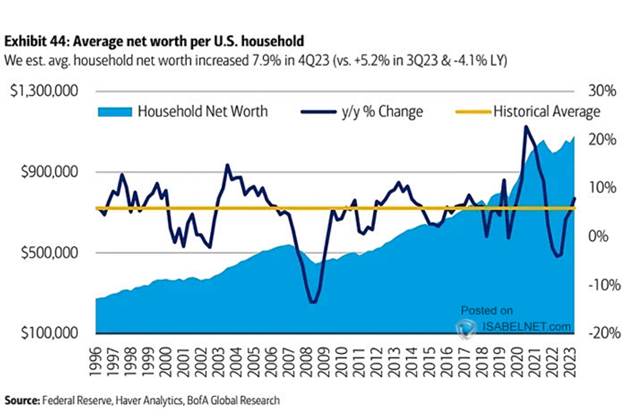

Household wealth in the United States reached a record of approximately $156 trillion by the end of 2023. It increased by about 3.2% from October to December. At the end of 2019, it was $110 trillion, representing a growth of over 40% in 4 years!

Household deleveraging has partly occurred at the expense of the state, which has become poorer due to Covid. Despite the rate hikes, the Fed still struggles to slow down growth. The temporary effects on inflation are now over, and the last mile to bring it back to the 2% target proves challenging. Lowering rates too aggressively could prove dangerous. By reigniting the credit machine, another wave of inflation could emerge even before the central bank’s target is reached.

The latest IMF report shows that the impact of the rate hike on real estate in the United States has been limited due to the loan structure (fixed rates). Real estate inflation is declining but very modestly and remains high.(https://www.imf.org/en/Publications/WEO/Issues/2024/04/16/world-economic-outlook-april-2024)

Households have adapted to higher interest rates offered on savings accounts and certificates of deposit, as well as money market mutual funds. In a way, the increase in interest rates now promotes household wealth growth, as real rates are now largely positive.

Real interest rates in the US at 5 and 10 years

Sources : Bloomberg, Richelieu’s Group

However, excessive tightening or maintaining higher rates for an extended period could pose a more significant risk. Over time, as mortgage rates reset, the transmission of monetary policy could suddenly become more effective and depress consumption at a sustained pace. Households may feel the effects, even where they have been relatively shielded so far.

If we look back simplistically since 2009, the decline in real rates has allowed for asset reflation for nearly 10 years to offset real estate losses on balance sheets. The level of negative real rates has led to increased leverage and thus wealth effects. In 2020, massive state aid in the US (and subsequent stimulus packages) triggered a rapid rise in household savings and led to deleveraging. Full employment following the lockdowns added to the wealth effect. A seemingly perfect sequence for households at first glance?

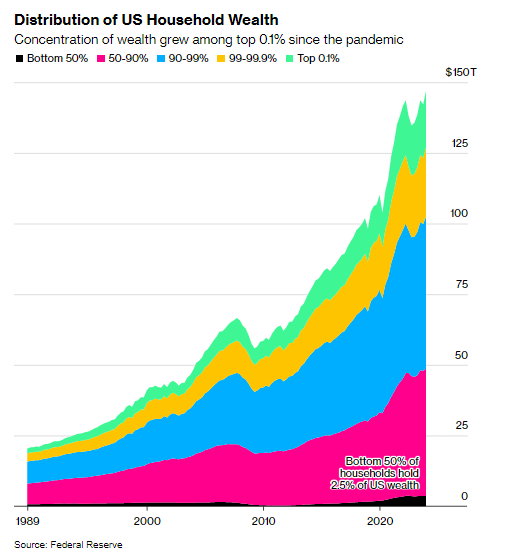

However, the landscape is less idyllic than it seems. Recall that out of the $37 trillion in additional wealth over the past four years, the distribution is concentrated among the top 0.1%. These 133,000 individuals shared about $20 trillion in wealth at the end of 2023, which amounts to roughly $150 million per household, according to Bloomberg.

The increase in rates has exacerbated and continues to exacerbate the imbalance… The higher the rates remain, the more the debt burden will increase, impacting the state’s budget deficit. The higher the rates remain, the more vulnerable economic agents (businesses and consumers) become entrenched. Meanwhile, the state becomes poorer, and systemic risks (commercial real estate, credit card defaults) increase. The US presidential elections in November should be a moment of tension crystallization.

Unlike Europe, American inflation remains linked to a demand shock and a robust economy. Economic slowdown is likely necessary to meet the central bank’s demands. So far, so good, but risks are increasing… just a few months away from the elections…

Raising rates is not a solution, and neither is a sharp decrease. It’s a delicate balancing act for the Fed, which must be patient and credible at the same time.

Perhaps its best interest would be to wait and keep its fingers crossed…

Macro-economic point

· American disinflation, which has been underway for several months, appears to be slowing down and casting doubt on the Fed’s future actions.

· The economic recovery in Europe is unlikely to deter rate cuts as early as June.

· The Bank of Japan does not foresee any changes in monetary policy.

· Chinese authorities are attempting to reassure regarding their ability to end the real estate crisis and restore some short-term confidence.

· The Indian momentum remains unchallenged.

UNITED STATES

The data released in the United States this month once again sent mixed signals. American growth remained robust. However, the factors that supported consumption and investment are gradually dissipating. American households’ room for maneuver has begun to shrink in the face of several headwinds: rising taxes, still restrictive financial conditions (particularly high credit card and mortgage interest rates), and depletion of savings accumulated during the pandemic. The prospects for a smooth landing of the US economy seem to be materializing. Tension in the job market appears to be gradually easing, with employers “no longer feeling pressured to hire” (according to the Beige Book) and an increase in the number of candidates per job opening.

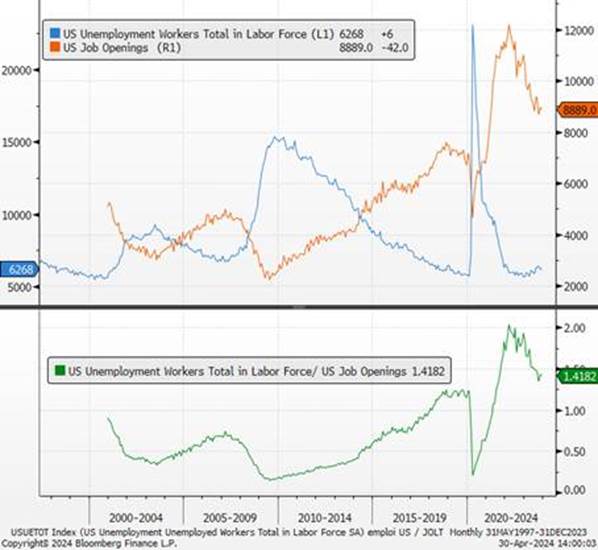

Job openings and number of unemployed in the United States

Sources : Bloomberg, Richelieu’s Group

We expect a slowdown in demand and thus a relapse in growth and inflation. For business investment, its dynamism is partly explained by the effects of the stimulus and investment plans implemented by Joe Biden in recent years (such as the Reduction Act of 2022 or the Bipartisan Infrastructure Law of 2021). This effect on GDP will diminish without new fiscal stimulus, which is highly unlikely in the coming months as the elections approach. In a context of slowing demand, business investment decisions are likely to be revised downwards, contributing less favorably to growth.

Jerome Powell aimed for greater confidence in inflation figures, but so far, this hasn’t materialized. However, we expect price increases to be more moderate in the second half of the year, allowing the Fed to lower interest rates. With a moderate slowdown on the horizon, the most likely date for the Federal Reserve to cut interest rates is now July or September. We maintain our forecast of two rate cuts (one in December) and a firm Fed commitment to restrain growth by keeping real rates high to avoid any uncontrolled return of inflation.

Core inflation figures over 12, 6, and 3-month periods

EUROPE

Europe continues its recovery. The release of preliminary PMI indices for April in the eurozone has sent a positive signal regarding the ongoing activity recovery. This momentum is mainly driven by the services sector (52.9 in April), while the manufacturing sector still faces challenging conditions. In the case of Germany, the release of the IFO indices has reassured all sectors of the economy, including manufacturing, which continues to recover. This will reinforce the hypothesis that the trough of activity in the eurozone has been surpassed and that the economic environment is tending towards normalization.

German economic indicators

Sources : Bloomberg, Richelieu’s Group

In this regard, while the improvement in European consumer confidence remains slow, it is expected to strengthen in the coming months alongside the rebound in real wages, which will support household consumption without bringing about inflationary pressure. Underlying inflation should show a slowdown due to a weakening of the wage-price spiral, as well as a lesser ability for businesses to raise prices in an economic environment that remains delicate after several quarters of demand contraction. The door is therefore clearly open to a first interest rate cut in June followed by a path of gradual easing.

Consumer confidence indicators

Sources : Bloomberg, Richelieu’s Group

The debate now shifts to the timing of further interest rate cuts. The ECB will be able to cut them four times this year.

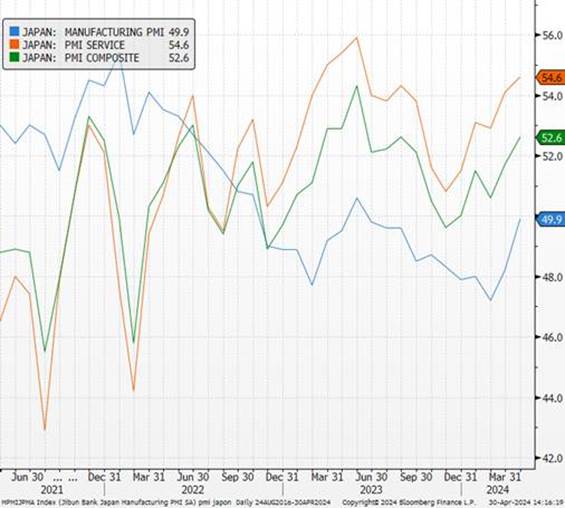

JAPAN

The Bank of Japan keeps its monetary policy unchanged, but maintaining a very dovish tone contrasts with many recent statements. The central bank’s modus operandi is confirmed: new rate hikes will only occur in the event of higher-than-expected inflation. The tourism sector remains very dynamic, with the number of visitors surpassing 3 million for the first time (visitor spending has increased by over 40% since 2019). Supported by the depreciation of the Yen, foreign trade is active, and the trade balance surprises with a positive balance of 366 billion. Exports remain strong, especially driven by semiconductors to China. Japanese business sentiment is strong (Tankan report). It’s worth noting that the central bank officially ended its ETF purchase program in March, while remaining the largest holder of Japanese equities with nearly 7% of the country’s market capitalization.

Economic indicators in Japan

Sources : Bloomberg, Richelieu’s Group

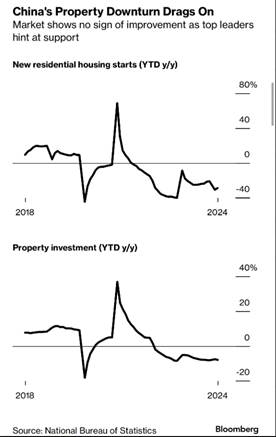

CHINA

Despite strong Chinese data in January and February, the slight downturn in March reinforces the need for fiscal and monetary support. Chinese policymakers are finally focusing on reducing housing inventories. The recent decline in home sales and prices has allowed for further measures to prevent a prolonged slowdown, which would harm household wealth and confidence. Growth has improved, but it is not the time to withdraw support. We should expect a continued recovery in infrastructure investments, but consumer weakness should remind us of the delicate economic situation and a worrying debt trajectory combined with a deflationary environment.

Consumer and producer prices in China

INDIA

Nearly a billion voters are heading to the polls to elect the 543 members of the lower house of the Indian Parliament (Lok Sabha). The third phase of India’s general elections (out of a total of seven) is scheduled for May 7, and the election results will be announced on June 4. The latest economic indicators affirm the country’s robust growth profile. Activity has continued to grow at a very strong pace, still driven by strong domestic and external demand. Over the month, price pressures have eased slightly, and employment in the manufacturing sector is increasing. With new demand engines coming from green energy and India’s manufacturing ambitions, the Capex theme is expected to continue to be the main driver of growth.

Economic indicators in India

Sources : Bloomberg, Richelieu’s Group

Asset allocation – Prioritizing flexibility in a volatile market

· Market volatility should present opportunities.

· We believe geopolitical tensions have peaked.

· We prefer to seek opportunities in more “value” segments in Europe.

· The hesitations of the Bank of Japan encourage us to stay out of this market.

· In the short term, China’s focus on reducing housing inventory could be a catalyst to prolong the recovery.

· If US 10-year rates exceed 5%, the correction would be significant.

· We favor the investment-grade (IG) segment and higher-quality high yield (HY) primarily in Europe.

GLOBAL ALLOCATION

The underlying macroeconomic backdrop remains positive as the global economy shows resilience. There is uncertainty regarding the decline in inflation given recent data. During the second week of April, we advised to be slightly more cautious on equity markets without changing our neutral outlook considering earnings releases.

We do not have ambitious targets for indices for the next six months. Doubt about central banks’ attitudes is likely to increase volatility, whether in equities or interest rates. As we approach the end of June, the fateful date for the beginning of rate cuts by the ECB or the Fed, the market is likely to stress over every inflation or price data release. However, we are convinced that as US growth slows, disinflation will materialize.

In the future, we believe geopolitical tensions have peaked, at least in the short term. None of the parties involved (the US, Israel, Iran) have an interest in an escalation that would spike oil prices and could cause a global recession. Even Russia may not be interested in dealing a major blow to the global economy as it is more dependent than ever on oil prices to fund its war economy. We are confident that growth concerns will outweigh inflation worries (which remain cyclical). In this perspective, bonds should be favored given the yields reached at the end of the month. Market volatility should present opportunities to be more flexible.

Global indices in local currencies

Sources : Bloomberg, Richelieu’s Group

EQUITIES

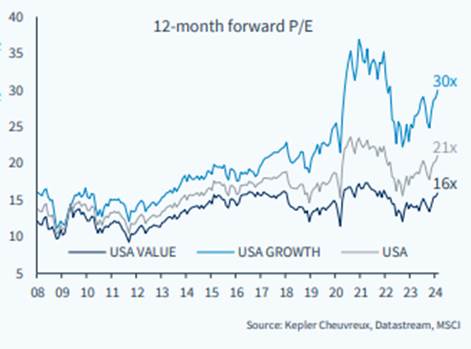

Valuations will come under pressure from the Fed’s commitment to maintaining restrictive policies despite still resilient earnings. The largest weights in US indices are expected to experience profit-taking in favor of other more cyclical sectors. We should see a sectoral rotation that allows indices to stabilize after a period of consolidation. However, if US 10-year rates exceed 5%, the correction would be significant. Some inflation caused by strong demand is actually favorable for corporate earnings growth. Positive figures announced on the US economy and profit forecasts have pushed US equity markets towards valuations that seem stretched to us, less compatible with a less accommodative Fed.

Valuation of the US market

The companies in the S&P 500 are experiencing the lowest average outperformance after positive earnings releases since the fourth quarter of 2020, despite still solid fundamentals. Small-cap US stocks continue to underperform due to their sensitivity to interest rates. Estimates of post-pandemic excess savings by the Federal Reserve suggest that they have now been depleted.

We prefer to seek opportunities in more “value” segments in Europe. Our conviction remains that European indices are best positioned in the current setup. PMI indices show a recovery in the private sector, driven by services benefiting from increased household purchasing power. Disinflation is more pronounced, and the ECB has far fewer questions to answer than the Fed. The ECB can afford to be the most accommodative central bank. Additionally, China’s stated desire to stabilize should favor the region overall, cyclical stocks, and Germany in particular. The UK, Europe’s most diversified index with a clearly defensive characteristic, can also be favored. The hesitations of the Bank of Japan lead us to stay out of this market. Even though the timing is uncertain, the fact that the BOJ has officially announced the end of ETF purchases, combined with our expectation of intervention in the Japanese currency, leads us to stay away.

Regarding emerging markets, currencies are expected to suffer from the strength of the dollar, favoring local currency-denominated equities. In the short term, China’s focus on reducing housing inventory could be a catalyst to prolong confidence and stock markets recovery, at least cyclically until structural weaknesses take over again. We remain positive on the Indian market given the growth dynamics and the lesser sensitivity of the Indian currency to the dollar. The INR is among the most resilient emerging market currencies and least correlated with the dollar.

Major equities markets

Sources : Bloomberg, Richelieu’s Group

SOVEREIGN BONDS

The major government bond markets have moved in concert in recent years, but we expect this to change in the future due to differences in debt fundamentals, monetary policy transmission, and fiscal support. Inflation in the United States remains largely cyclical, and the slowdown in growth towards the end of the year should favor disinflationary outlooks and allow for a decrease across the rate curve. This gives us a preference for US Treasuries over other government bond markets. Real interest rates are expected to remain high as inflation dynamics weaken. Our intervention level was between 4.3% and 4.5% on the US 10-year, and current levels are even more attractive given our growth slowdown scenario. At its latest meeting, the Fed announced that from June 1, it would reduce the cap on Treasury securities allowed to mature and not be replaced to $25 billion, while the current cap is $60 billion per month. This is clear evidence that Jerome Powell does not want much higher levels on government interest rates. Our year-end outlook at 3.8% is raised to 4.1% (the same for the 5-year).

Sovereign 5-year rates

Sources : Bloomberg, Richelieu’s Group

CREDIT

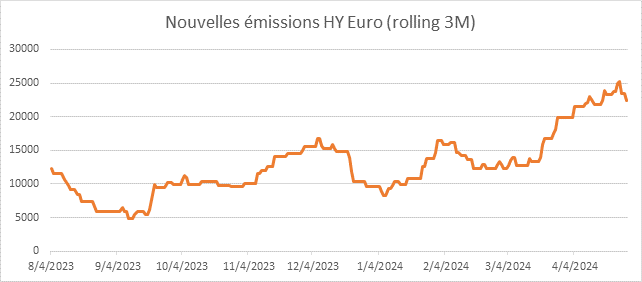

We are constructive on duration, especially in Europe given the recent rise in yields and the accommodative tone of the ECB. For corporate credit, we prefer quality and securities with maturities of 2 to 5 years in Europe and the United States. We are also positive on select emerging markets while remaining cautious of short-term dollar strength, preferring other funding currencies. There is increasing dispersion within the credit asset class itself, notably in high yield (HY) with the recent confirmation of difficulties for some issuers weighing heavily on the market (Altice, Atos, Intrum, Ardagh, or Grifols). Many small-sized and poorly-rated (B-/CCC) issuers are also in distress. The risk for the most indebted issuers is even greater as rates remain high for longer, making refinancing difficult. This situation underscores the importance of being selective and sufficiently compensated, in terms of spreads, to address these challenges. We favor the investment-grade (IG) segment and higher-quality high yield. Unlike distressed issuers, these better-rated issuers have benefited from relatively tight spreads for refinancing since the beginning of the year, evidenced by a record level of issuance in the BB segment. We remain cautious on US high yield. We believe the market has not yet fully priced in the impact of high rates for an extended period. The most vulnerable players will face increasing financial pressures.

Credit spreads

Sources : Bloomberg, Richelieu’s Group

New Euro High Yield Issues (rolling 3M)

Sources : Bloomberg, Richelieu’s Group

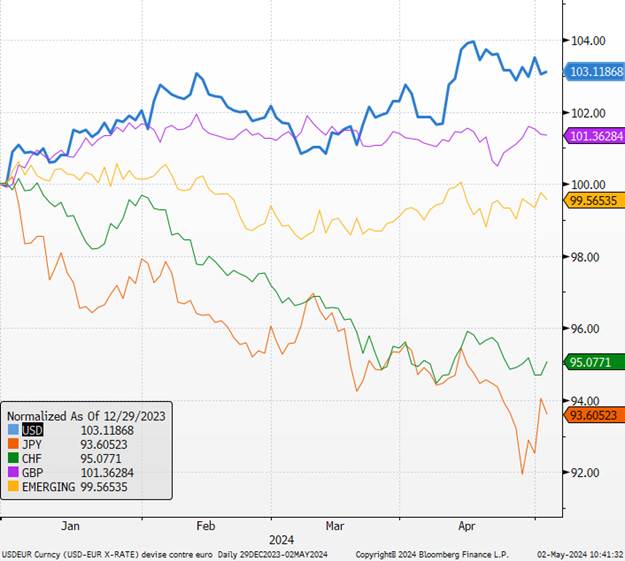

CURRENCIES

The dollar is expected to remain strong in the short term as the prospects for rate cuts in the United States diminish while those for the ECB remain. We anticipated a strengthening of the US currency since February to account for the adjustment of expectations regarding the central bank’s rates. This has been realized. The latest publications show strong resilience in the economy, both in terms of real estate and employment, providing some support until the summer. We anticipate a revaluation of the euro in the second half of the year as the market factors in slower US growth (targeting 1.12 in 12 months).

Currencies against EURO (Base 100 as of 31/12/2023)

Sources : Bloomberg, Richelieu’s Group

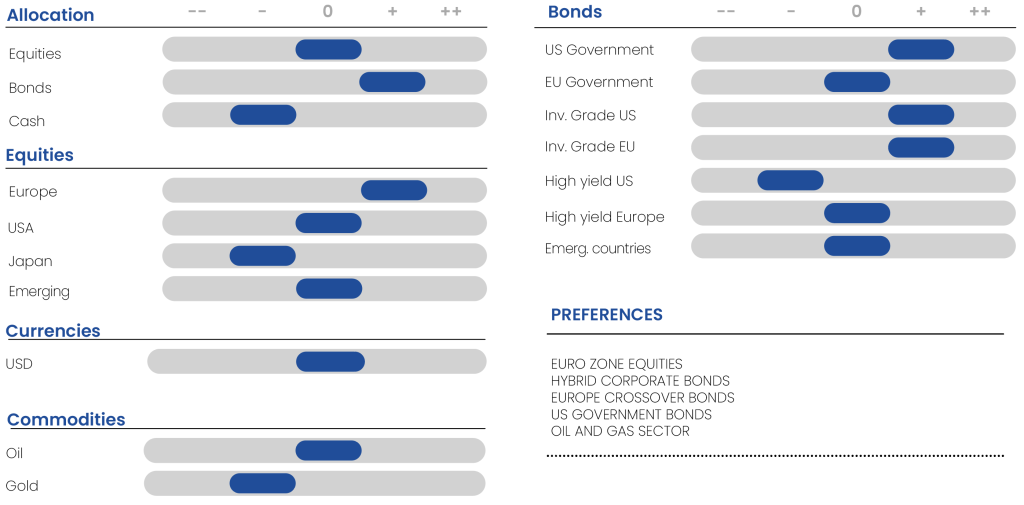

Asset Allocation Table

Synthesis Strategy Richelieu Group – Author

Alexandre HEZEZ

Group Strategist

Disclaimer

This document was produced by Richelieu Gestion, a management company and subsidiary of Compagnie Financière Richelieu. This document may be based on public information. Although Richelieu Gestion makes every effort to use reliable and complete information, Richelieu Gestion does not guarantee in any way that the information presented in this document is reliable and complete. The opinions, views and other information contained in this document are subject to change without notice.

This document was produced by Richelieu Gestion, a management company and subsidiary of Compagnie Financière Richelieu. This document may be based on public information. Although Richelieu Gestion makes every effort to use reliable and complete information, Richelieu Gestion does not guarantee in any way that the information presented in this document is reliable and complete. The opinions, views and other information contained in this document are subject to change without notice.

The information, opinions and estimates contained in this document are for information purposes only. No element can be considered as an investment advice or a recommendation, a canvassing, a solicitation, an invitation or an offer to sell or to subscribe to the securities or financial instruments mentioned. The information provided concerning the performance of a security or financial instrument always refers to the past. Past performance of securities or financial instruments is not a reliable indicator of future performance.

All potential investors should conduct their own analysis of the legal, tax, accounting and regulatory aspects of each transaction, if necessary with the advice of their usual advisors, in order to be able to determine the benefits and risks of the transaction and its appropriateness to their particular financial situation. He does not rely on Richelieu Gestion for this.

Finally, the content of the research or analysis documents or their excerpts, if any, attached or quoted, may have been altered, modified or summarized. This document has not been prepared in accordance with the regulatory provisions designed to promote the independence of financial analysis. Richelieu Gestion is not prohibited from trading in the securities or financial instruments mentioned in this document prior to its publication.

Market data is from Bloomberg sources.