A precarious balance between growth risk and gradual disinflation.

By Alexandre Hezez, Group Strategist

Editorial

Inflation seems to be under control : we are witnessing a slow, steady deceleration in price rises in the United States. Monetary tightening appears to be coming to an end. The rise in goods prices has been decelerating sharply for over a year, starting with raw materials and energy products. Even as disinflation takes hold, the dynamics remain very different, leading to a decoupling of the economies.

Graph : Core inflation (inflation excluding energy and food)

Sources: Bloomberg, Richelieu Group

Globally, we expect average annual real GDP growth to slow to 2.6% year-on-year in 2023, driven by tighter monetary policy and tighter bank lending in the US and Europe. Slower growth in China is also likely to weigh on global activity. We expect global core inflation to fall below 3% in 2024, reflecting supply chain improvements and slower wage growth.

United States: disinflation well underway

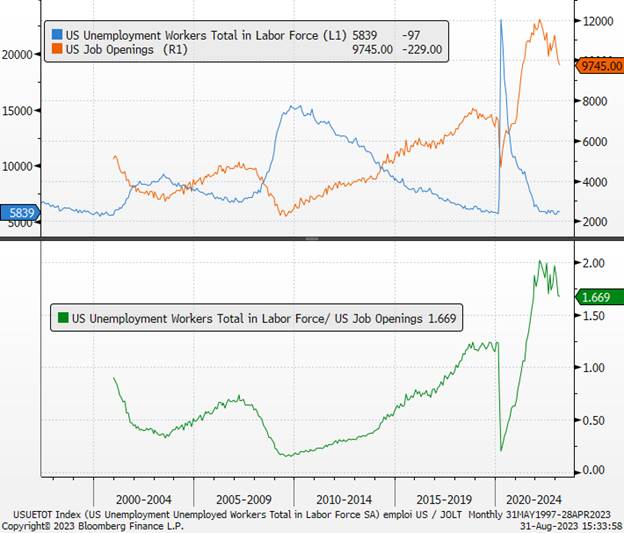

We expect core inflation to fall to 3.5% by December 2023, reflecting the continued recovery of the supply chain, lower housing inflation and a slowdown in services inflation as wage growth continues to moderate. Normalization of the job market is underway, as the latest data published (Job Openings, ADP report) demonstrate.

Graph : number of job offers versus total jobs

Sources : Bloomberg, Groupe Richelieu

We anticipate a slight deterioration in the unemployment rate towards the end of the year. This phenomenon will not be sufficient to have a tangible impact on wage dynamics. We believe that the Fed’s rate hike cycle is now over, and that it will maintain the current federal funds rate range of 5.25% to 5.5% until 2024. We do not expect the first rate cut to take place before the end of the second quarter (25 bp), while remaining on the alert for inflation.

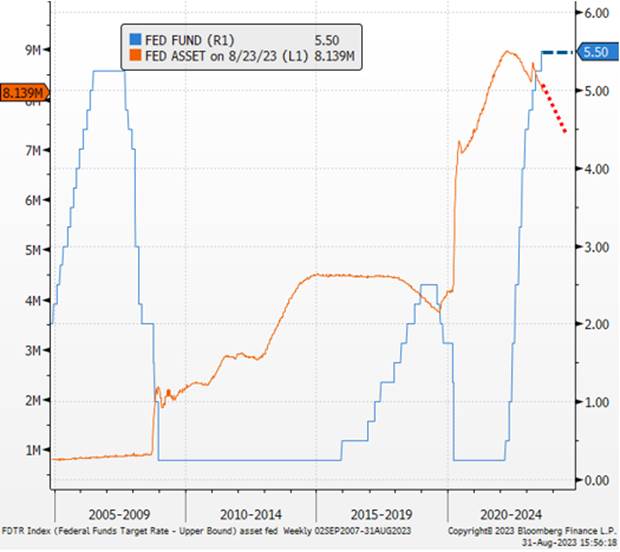

Chart : Fed Fund / Fed balance sheet & estimate

Sources : Bloomberg, Groupe Richelieu

At the risk of repeating ourselves, we are convinced that the Fed will continue, whatever happens, to keep up the pressure to avoid a resurgence in inflation. In August 2022, Jerome Powell’s speech at the Jackson Hole central bankers’ conference already stressed his frank intention to “vigorously use all its tools” and ” before concluding that “fighting inflation in the United States will hurt American households and businesses, but giving up would be even more damaging for the economy”. For the time being, this is not the case. Paradoxically, the resilience of the US economy could henceforth be a source of stress for central bankers and markets alike.

Europe: the risk of stagflation returns

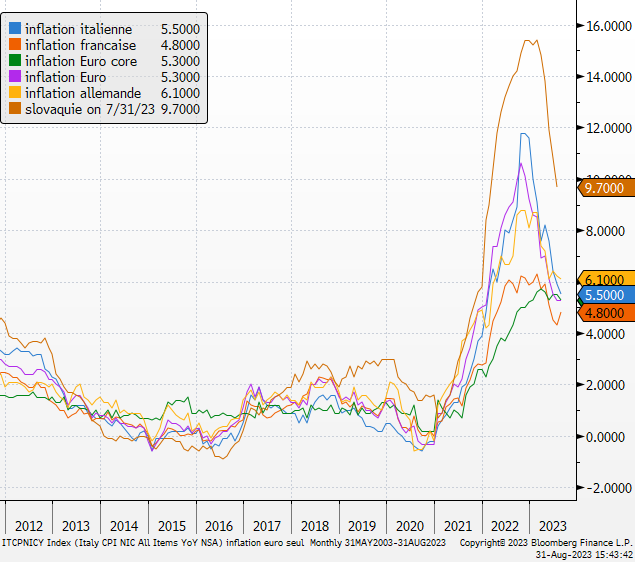

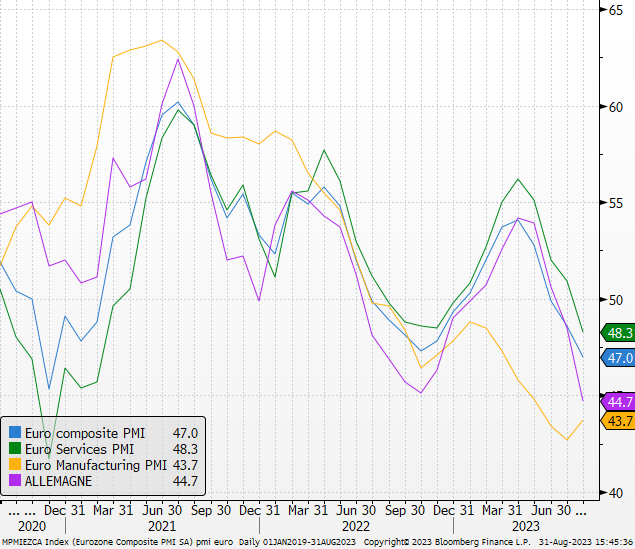

Inflationary pressures will continue to prevail. Preliminary inflation data for August in Germany, Spain and France offered little reassurance that eurozone inflation is slowing. The movement will be slow and gradual, and will continue to open the door to the end of key rate hikes by the ECB at the end of the year. PMIs showed that the European economy weakened, driven mainly by services. These figures underline a weakening in demand and the impact of monetary policy tightening on the economy.. European growth stalled over the summer. In the Eurozone, we expect GDP growth to slow to 0.6% in 2023, reflecting historically high energy prices due to the war in Ukraine, tighter bank lending standards. We expect core inflation to fall gradually to 4.0% year-on-year by the end of 2023, reflecting the indirect pass-through of lower energy and food prices, although we expect services inflation to remain high due to the tight labor market.

Graph: Headline inflation in the Eurozone

Sources : Bloomberg, Groupe Richelieu

We expect the ECB to carry out two further hikes (25 bp) in September and December, for a terminal rate of 4.50/4.75, given vigorous underlying inflation, driven by services. Thereafter, we believe that the ECB will remain on standby for 2024, even if we forecast a worsening European economy. Christine Lagarde can only remain unmoved until inflation is anchored on her 2% target. A China that is struggling to rebound will affect global growth, and in particular the more dependent European economy. Despite worrying figures, the risk of recession will not be taken into account for the time being by the ECB, which has not yet succeeded in regaining control of inflation. A more rapid reduction in the ECB’s balance sheet is likely to be the subject of debate, with reference to a possible halt to reinvestments of securities acquired under the Pandemic Purchase Program (PPP), which are nevertheless scheduled to run until the end of 2024 by the Governing Council. Indeed, the reduction in underlying inflation is less advanced than in the United States.

In Jackson Hole, Christine Lagarde underlined the persistence of several sources of uncertaintyThese include those that could structurally lead to higher inflation than in the past (increased investment needs and supply constraints linked to climate change, stronger bargaining power for employees, and the ability of companies to raise prices more quickly). For the ECB, reaching these targets could require a significant slowdown in activity, due to the relentless determination of central banks “to kill the beast” (Gita Gopinath, IMF Deputy Managing Director). In Europe, we are seeing a return to the risk of stagflation.

Graph : Eurozone economic indicators

Sources : Bloomberg, Groupe Richelieu

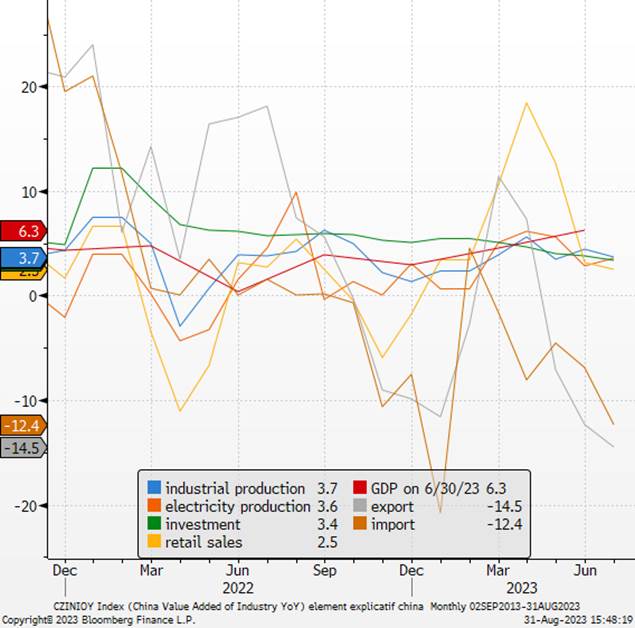

China: deflation on the horizon

The Chinese economy has not rebounded as expected, despite three years without containment due to the pandemic. The limited pace and scale of fiscal and monetary support measures failed to stimulate growth. Medium-term challenges such as demographics, the persistent real estate slowdown, government indebtedness and geopolitical tensions could weigh on future growth.

Graph : explanatory factors for Chinese growth

Sources : Bloomberg, Richelieu Group

These factors are compounded by delays in property payments and a flood of local debt obligations. To stimulate demand, China is acting cautiously. A minor improvement in monthly statistics could allay concerns. PMI indices for August were slightly positive, indicating expansion. However, real estate instability suggests a long way to go before a beneficial impact. We anticipate GDP growth of 5.4% in 2023, following the post-opening recovery. Although current data is lacklustre, we expect sequential growth in H2 thanks to a reduction in the effect of destocking, the intensification of easing measures and the stabilization of exports. The central bank will intensify monetary support, while limiting the impact on the foreign exchange and real estate markets. Previous stimulus plans have led to harmful speculative bubbles. Although worrying in the short term, this situation could be reversed with the end of the Fed’s aggressive policy. China’s central bank is expected to cut rates to stimulate consumption and investment. The timing remains uncertain. Beijing avoids increasing indebtedness, particularly at local level, due to systemic risk. Options are scarce, but efforts are needed to achieve 5% growth.

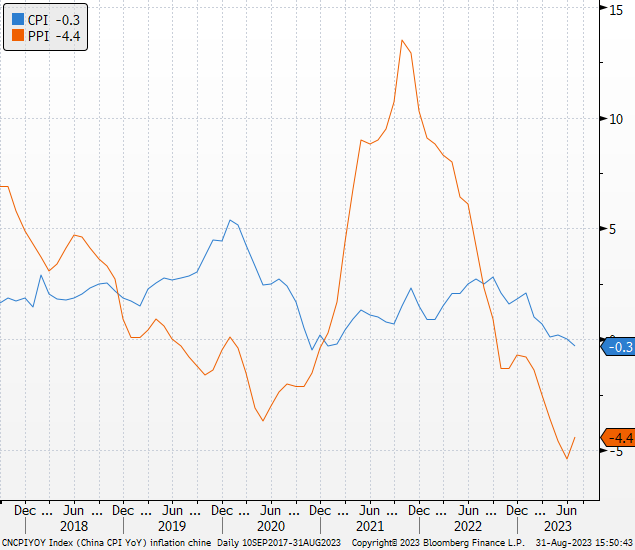

A delicate situation for the world

Current challenges are prompting us to readjust our forecasts for China. Negative data for June could lead to further stimulation of domestic demand by the end of the year. Faced with weakened global trade and Western sanctions, China is looking for growth levers. Lower growth may influence global disinflation, especially for raw materials, but it is also likely to have an impact on Europe.

Graph : consumer prices versus producer prices

Sources : Bloomberg, Groupe Richelieu

Uncertainty surrounds the real estate slowdown, perceived as a major economic threat. The situation in China is bound to have an impact on global growth. Although detrimental on a global scale, China’s difficulties have one short-term advantage: they are easing inflationary pressures in the United States and Europe. Unlike the rest of the world, China does not suffer from inflation. Pending a recovery in industry, its weakness is helping to curb inflation. Conversely, a rebound at the end of the year could stimulate it, putting the ECB in a tricky position. If China continues to decline, this will affect the global economy. A a complex situation for the United States, faced with a weakening adversary. Too much weakening of China risks upsetting the global economic balance. US Commerce Secretary Gina Raimondo’s visit to China reflects these concerns. The two superpowers, seeking to reduce tensions, stepped up their meetings.

The Fed is no longer an insurance policy against the crisis

Global growth momentum is mainly driven by the US macro-economic cycle. The full impact of the aggressive monetary tightening of 2022 could soon be felt. In previous downturns, the Fed has always acted to support the economy.

We remember, in 2019, the reversal of US monetary policy during the trade war between Trump and China after a steady rise in rates in 2018. COVID has obviously left its mark on us all. We all remember the crisis of 2007 (although fewer of us do…). This time, the situation is different: the US economy is one of the most resilient. Growth expectations have been raised throughout 2023 and US growth is more robust.

Western consumers have seen their purchasing power dwindle, affecting their morale and their ability to consume. The savings built up during the confinements served as a cushion. Nevertheless, the scale and duration of the price rises are raising fears of a fall in consumption. Wage demands remain high, especially in Europe and the United States, even though employment is deteriorating. Continued wage inflation will impact the actions of central banks and businesses alike. Household consumption, which accounts for around two-thirds of GDP, is seen as the driving force behind this dynamic, with Americans continuing to spend at a steady pace to date. While they face a resumption of student loan repayments and high borrowing costs in the months ahead, a strong job market should continue to boost their spending. A scissor effect could occur if employment deteriorates.

The ability of American households to acquire real estate has never been so low, which presupposes a fall in real estate prices or wage restraint.

Households’ ability to buy real estate

Source : X (formerly Twitter)

If China gets bogged down and Europe becomes entangled in unmanageable inflation, being forced to adopt a restrictive monetary policy despite the risks (slower growth, Ukraine, gas, China), US monetary policy will not compensate. Worse, it will continue to do so by lowering its balance sheet over the coming months. Jerome Powell’s obsession remains the fear of the 1970s, with its successive waves of inflation. Central banks cannot let up. The risk of a global recession is increasing, while at the same time the US economy remains resilient. There’s nothing to expect from the FED (or the ECB) as in previous crises.

After a start to the year which saw a gradual decline in risks (gas restocking in Europe, reopening of the Chinese economy, effective disinflation in the United States), the coming months could well see a resurgence of risks on these same themes. Geopolitics remains a key factor to watch. In Europe, tensions with Russia remain high, particularly over Ukraine. Sanctions, trade wars and rising nationalism could hamper global growth a year ahead of the US presidential elections. Until China demonstrates its ability to manage the real estate crisis and return to sustainable growth, the macroeconomic balance will remain fragile.

Asset allocation

CHINA, CORPORATE MARGINS, INFLATION…

Central banks cannot let up. The risk of a global recession is increasing, while at the same time the US economy remains resilient. The decoupling of economies has intensified over the past month. The defensive positioning of investors at the start of the year and the resilience of the economy despite rising interest rates are the two pillars supporting equity markets. Geopolitics remains a key factor to watch. In Europe, tensions with Russia are still palpable, particularly around Ukraine. Sanctions and trade wars could hamper global growth a year ahead of the US presidential election. Until China demonstrates its ability to manage the real estate crisis and return to sustainable growth, we will remain vigilant.

Equities

We have lowered our short-term equity outlook from neutral to underweight, taking into account uncertainties related to China, European monetary policy and pressure on corporate margins.

Chart : Year-to-date performance of equity indices

Sources : Bloomberg, Groupe Richelieu

The market is now adopting a “bad news is good news” approach. Negative employment and corporate indicators were well received by investors. A few years ago, this would have been justified, as central banks sought to support growth in an inflation-free environment. The market wants to be convinced that if macroeconomic data deteriorates, central banks will revise their monetary policy. We’re convinced of the opposite.

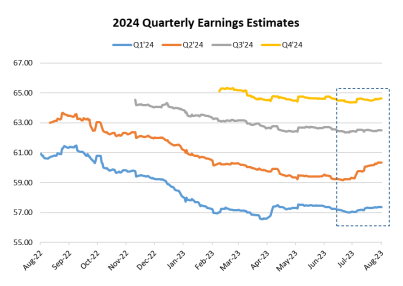

Over the next few quarters, the fall in inflation, which had benefited companies, will lead to a more marked slowdown in nominal growth than in real economic growth. Production costs will remain high, and wage growth will not decline as rapidly as nominal growth. Corporate profit margins could therefore come under pressure.

Chart : Quarterly earnings estimates for S&P companies

Source : Raymond James

Consumers resisted the rise in interest rates and the loss of purchasing power, thanks to a solid job market. The deterioration of the latter will have a negative impact on the economy, especially as wages will remain at the heart of demands, as illustrated by the current negotiations between the powerful United Auto Workers union and Ford on wage increases. The union is demanding +45%, while the manufacturer is proposing +15%.

The economic downturn, coupled with increasingly restrictive central bank policies, has prompted us to adopt a cautious stance on European equities. The risk of a contraction in bank lending will encourage investors to favor quality defensive stocks over cyclicals. This rotation is also fuelled by falling PMI indicators.

The services dynamic in Europe, which is still driving growth, is gradually running out of steam. This will lead to below-potential growth in the eurozone over the next few quarters, but not enough to win the battle against inflation. China will continue to weigh on European corporate earnings, particularly in the capital goods sector.

Corporate results showed some resilience, including in Europe, although they were more mixed this time around, starting from low expectations.

As a general rule, we will avoid companies with too high a debt ratio. The preferred geographic segment remains the United States for its visibility and . It’s now a little complacent to think that the markets’ new macro scenario of reflation doesn’t anticipate the ever-present risk of recession at all. It expects earnings growth to accelerate, which seems optimistic to us.

With regard to emerging countries, and China in particular, we have taken note of further setbacks in the property sector and have lowered our positive outlook.However, after the meeting of the Politburo, the Chinese Communist Party’s governing body, which confirmed the intensification of economic measures, the equity markets reacted very well. Given the current stakes, Beijing’s measures to stimulate growth remain moderate, reflecting the authorities’ caution in the face of financial risks. Defending our currency remains our top priority.

As long as Chinese growth shows no tangible signs of recovery, caution will prevail in risky assets. We are convinced that stimulus measures will take shape, but the timing is uncertain. We are not negative on the Chinese market, as we believe that the leverage is much greater in terms of performance, given the valuations and already significant capital outflows in the region.

Themes and sectors

In sector terms, we are focusing on defensive stocks rather than cyclicals which benefited from a readjustment in the economic outlook during the first half of the year. This rotation seems to show that investors realize that a lot of good news has already been priced in. From now on, a further rise in the market will become more difficult. The macroeconomic environment is not simple, and it will become more complicated for companies to defend margins that are at historically high levels. Large technology companies are benefiting from the as yet untapped prospects of AI. The banking sector remains highly resilient in this environment. The themes of relocation and energy transition remain at the heart of our portfolio.

Rates & Credit

Bond segments continue to deliver appreciable profitability, despite rising bankruptcies. We favor quality assets in all segments. We favor short durations and the most balanced segments in terms of risk/return (BBB/BB). We believe there could be some rate pressure to exploit during the quarter. We have upgraded our view on bonds, in view of the rate hikes that took place over the summer months. We expect rates to stabilize again as growth weakens. Now that yields on 10-year US Treasuries have risen above 4%, we can build up positions in US sovereign bonds to diversify and protect the portfolio in the event of a major crisis.

Chart : Year-to-date bond index performance

Sources : Bloomberg , Groupe Richelieu

As for corporate bonds, we have seen a striking and undifferentiated tightening of credit spreads. Although this may indicate that investors see the current macroeconomic environment as positive for carry trades, we are more selective.

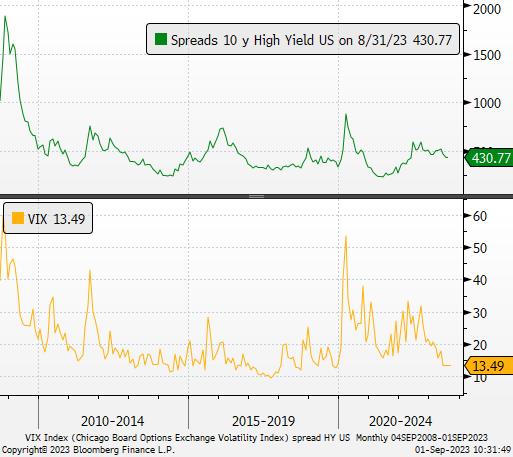

As rates rise in the US, higher interest charges could lead to market tensions and waves of defaults by the most indebted companies, particularly in commercial real estate and the private market. The credit industry is underestimating the current level of macroeconomic uncertainty, and the risk of corporate default is bound to increase. Equity volatility is set to increase, driving up spreads. We are reducing our conviction in US High Yield after the sector’s good performance.

Chart : US HY spreads versus implied equity market volatility (VIX)

Sources : Bloomberg , Groupe Richelieu

Overall, interest rates will remain high and, as in previous cycles, we cannot count on rate cuts and hence substantial price appreciations. Coupon yield remains the main interest for these investments. Taking into account curve inversions, we recommend short terms (3 to 4 years).

Currencies & commodities

As for the dollar, we reached our first target in July (1.12). We continue to believe that the euro should appreciate against the dollar towards the end of the year. In recent months, the euro-dollar exchange rate has been strongly linked to the spread between short-term interest rates in the United States and Europe. This gap was very wide before the start of the European Central Bank’s rate hike cycle a year ago, but has narrowed steadily since. Recently, there have been offensive statements from some FOMC members and economic data showing the US economy to be holding up well. However, this should be temporary, as the ECB needs to catch up with the Fed, given Christine Lagarde’s persistent determination.

Graph : 2-year USD/EUR versus USD-EUR swap differential

Sources : Bloomberg, Groupe Richelieu

Thanks to these factors and OPEC+’s efforts to reduce oil supply, the price of Brent crude has moved closer to our $90/b target. While the positive catalysts took time to manifest themselves, their impact is now embedded in the market, limiting the upside potential of oil prices. We recommend caution, as the economic slowdown is set to continue, affecting the commodities market. After a long period of hesitation, Russia finally seems determined to meet its OPEC+ commitments, as reflected in the marked reduction in its oil exports. Saudi Arabia, as a partner and leader within OPEC+, has also played a crucial role in voluntarily reducing its production. US oil production remains stable, a sign of the caution shown by local producers. Furthermore, no agreement on the Iranian nuclear issue is expected, although Iran continues its unofficial exports, providing useful additional supply for the market. Global oil demand is set to reach an all-time high in 2023. China will make a massive contribution to this growth, despite recent signs of normalization. US demand is also robust, supported by positive economic data. The energy sector should benefit from a stabilization in oil prices. This framework could be a further catalyst for the sector, especially with recent dividend increases and share buybacks.

Graph : Brent and ural crude oil prices

Sources : Bloomberg, Groupe Richelieu

Allocation table

Synthesis Strategy Richelieu Group – Author

Alexandre HEZEZ

Group Strategist

Disclaimer

This document was produced by Richelieu Gestion, a management company and subsidiary of Compagnie Financière Richelieu. This document may be based on public information. Although Richelieu Gestion makes every effort to use reliable and complete information, Richelieu Gestion does not guarantee in any way that the information presented in this document is reliable and complete. The opinions, views and other information contained in this document are subject to change without notice.

This document was produced by Richelieu Gestion, a management company and subsidiary of Compagnie Financière Richelieu. This document may be based on public information. Although Richelieu Gestion makes every effort to use reliable and complete information, Richelieu Gestion does not guarantee in any way that the information presented in this document is reliable and complete. The opinions, views and other information contained in this document are subject to change without notice.

The information, opinions and estimates contained in this document are for information purposes only. No element can be considered as an investment advice or a recommendation, a canvassing, a solicitation, an invitation or an offer to sell or to subscribe to the securities or financial instruments mentioned. The information provided concerning the performance of a security or financial instrument always refers to the past. Past performance of securities or financial instruments is not a reliable indicator of future performance.

All potential investors should conduct their own analysis of the legal, tax, accounting and regulatory aspects of each transaction, if necessary with the advice of their usual advisors, in order to be able to determine the benefits and risks of the transaction and its appropriateness to their particular financial situation. He does not rely on Richelieu Gestion for this.

Finally, the content of the research or analysis documents or their excerpts, if any, attached or quoted, may have been altered, modified or summarized. This document has not been prepared in accordance with the regulatory provisions designed to promote the independence of financial analysis. Richelieu Gestion is not prohibited from trading in the securities or financial instruments mentioned in this document prior to its publication.

Market data is from Bloomberg sources.